Options on stocks were first traded on an organized exchange in 1973. Since then there has been a dramatic growth in options markets. Options are now traded on many exchanges throughout the world. Huge volumes of options are also traded over the counter (OTC) by banks and other financial institutions. The underlying assets include stocks, stock indices, foreign currencies, debt instruments, commodities and futures contracts.

There are two basic types of options. A call option gives the holder the right to buy the underlying asset by a certain date for a certain price. A put option gives the holder the right to sell the underlying asset by a certain date for a certain price. The price in the contract is known as the exercise price or strike price. The date in the contract is known as the expiration date or maturity. American options can be exercised at any time up to the expiration date. European options can be exercised only on the expiration date itself.

It should be emphasized that an option gives the holder the right to do something. The holder does not have to exercise this right. This fact distinguishes options from forwards and futures, where the holder is obligated to buy or sell the underlying asset.

Example 1

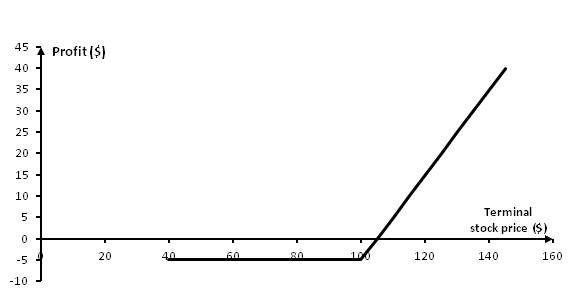

Consider the situation of a trader who buys one European call option contract of APPLE stock with a strike price of $100 (that is, the trader purchases the right to buy 100 APPLE shares for $100 each). Suppose that the current stock price is $96, the expiration date of the option is in two months, and the option price is $5. Because the options are European, the trader can exercise only on the expiration date. If the stock price on this date is less than $100, the trader will clearly choose not to exercise. (There is no point in buying for $100 a stock that has a market value of less than $100.) In these circumstances the trader loses the entire initial investment of $500.

If the stock is above $100 on the expiration date, the option will be exercised. Suppose, for example, that the stock price is $115. By exercising the options, the trader is able to buy 100 shares for $100 per share. If the shares are sold immediately, the trader makes a gain of $15 per share, or $1,500, ignoring transaction costs. When the initial cost of the options is taken into account, the net profit to the trader is $10 per option, or $1,000.

The following figure shows the way in which the trader’s net profit or loss per option varies with the terminal stock price. Note that, in same cases, the trader exercises the options but takes a lose overall. Consider the situation when the stock price is $103 on the expiration date. The trader exercises the options but takes a loss of $200 overall. This is better that the loss of $500 that would be incurred if the options were not exercised.

Figure: Profit from buying an APPLE European call option: option price = $5, strike price = $100

Example 2

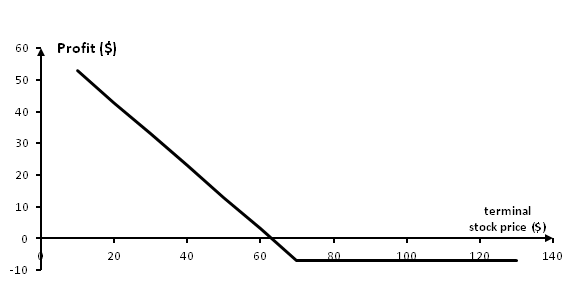

Whereas the purchaser of a call option is hoping that the stock price will increase, the purchaser of a put option is hoping that it will decrease. Consider a trader who buys one European put option contract on Exxon with a strike price of $70 (that is, the trader buys the right to sell 100 Exxon shares for $70 each). Suppose that the current price is $64, the expiration date of the option is in three months, and the option price is $7. Because the options are European, they will be exercised only if the stock price is below $70 at the expiration date. Suppose that the stock price is $50 on this date. The trader can buy 100 shares for $50 per share and, under the terms of the put option, sell the same shares for $70, to realize a gain of $20 per share, or $2,000. (Transaction costs are ignored). When the initial cost of the option is taken into account, the trader’s net profit is $13 per option, or $1,300. Of course, if the final stock price is above $70, the put option expires worthless and the trader loses $7 per option, or $700. The following figure shows the way in which the trader’ profit or loss per option varies with the terminal stock price.

Figure: Profit from buying an Exxon European put option: option price = $7, strike price = $70

Options Positions

There are two sides to every option contract. On one side is the trader who has taken the long position (i.e., has bought the option). On the other side is the trader who has taken a short position (i.e., has sold or written the option). The writer of an option receives cash up front but has potential liabilities later. The writer’s profit or loss is the reverse of that for the purchaser of the option.

Characteristic features

Definition

With an option the buyer acquires the right but not the obligation, against immediate payment of the option premium, to purchase (call option) or sell (put option) a certain quantity of the underlying instrument at a price stipulated in advance, either at any time during the life of the contract (American option) or on expiry date (European option).

By contrast, the writer of an option undertakes to deliver/sell (call option) or accept/buy (put option) the corresponding underlying instrument at the agreed price (striking price) if the option is exercised. Depending on the contract specifications, cash settlement can also be accepted in lieu of physical delivery.

The following may serve as underlying instruments:

- physical assets (equities, futures, bonds, commodities, precious metals)

- benchmarks (currencies, interest rates, indices)

American-style options: It is possible to exercise American-style options on any trading day up until the expiration date.

European-style options: It is only possible to exercise European-style options on their expiration date. This does not, however, limit their tradability on the secondary market (e.g. on a stock exchange).

Asian-style option: It is a variant of the European-style option. Alternatively referred to as an “average price” option, in an Asian-style option the reference price in relation to the underlying securities is derived from an agreed upon calculation, which, by way of example, may be based upon an average of the underlying securities’ market prices at predetermined dates occurring during a specified “averaging period,” with the exercise date (assuming the counterparty is the option buyer or holder) occurring at the end of such averaging period.

The investor should be aware that the calculation of an average value for the underlying securities in the case of the average-rate option can result in the value of the option on the expiration date being considerably lower for the buyer and considerably higher for the writer than the difference between the strike price and the current market value on expiry. For an average-strike option, the average strike price of a call option can be considerably higher than the price originally agreed. For an equivalent put option, the strike price can similarly be lower than the price originally agreed.

Currency option: A currency option gives its purchaser the right, but not the obligation, either to buy from the option writer, or to sell to the option writer, a stated quantity of foreign currency at a specified rate of exchange, on a given future date or at any time up to and including that given date. If the option is not exercised by this given date the agreement conferred upon the holder is deemed to have lapsed. If the holder has purchased the right to buy a foreign currency it is referred as a call option. If the holder has purchased the right to sell foreign currency it is referred to as a put option.

“In the money”, “out of the money” and “at the money” options:

A call option is “in the money”, i.e. has an inherent value, if the current market value of the underlying instrument is higher than the striking price. A put option is “in the money” if the current market value of the underlying instrument is lower than the striking price. An option that is “in the money” is said to have an intrinsic value.

A call option is “out of the money” if the current market value of the underlying instrument is lower than the striking price. A put option is “out of the money” if the current market value of the underlying instrument is higher than the striking price.

Call and put options are “at the money” if the current market value of the underlying instrument and the striking price are the same.

- Premium: The amount paid for the contract initially

- Underlying (asset): The financial instrument on which the option value depends.

- Strike (price) or exercise price: The amount for which the underlying can be bought (call) or sold (put)

- Expiration (date) or expiry date: Date on which the option can be exercised or date on which the option ceases to exist or give the holder any rights.

- Intrinsic value: The payoff that would be received if the underlying is at its current level when the option expires. (Difference between strike price and stock price)

- Time value: Value that the option has above its intrinsic. Uncertainty surrounding the future value of the underlying asset means that the option value is generally different from the intrinsic value.

- Long position: A positive amount of a quantity, or a positive exposure to a quantity

- Short position: A negative amount of a quantity, or a negative exposure to a quantity. Many assets can be sold short, with some constrains on the length of time before that must be bought back.

Value/Price of an option

The price of an option depends on its intrinsic value and on what is referred to as the time value. The latter depends on a variety of factors, especially the remaining life of the option and the volatility of the underlying. The time value of an option reflects the chance that it will be in the money. Hence, the time value is higher for options with a long duration and a very volatile underlying. The same is true for options that are at the money.

Categories

Traded options are financial instruments whose contract sizes, striking prices and expiry dates are standardized and which are traded on exchanges.

Over-the-counter (OTC) options transactions are contracts with standardized contractual terms or contract specifications agreed upon individually between buyers and writers. OTC options transactions are neither securitised nor traded on-exchange.

Warrants are non-standardized financial instruments. Warrants are options in securitised form. Some of them are traded on exchanges but many are traded over-the-counter.

Margin requirement/Margin cover

A margin is fixed for sales of puts and short sales of calls when the contract is concluded. This margin is recalculated periodically during the entire life of the contract and may result in equivalent margin calls.

In the case of traded options these margins and their calculation are subject to the guidelines laid down by the exchange in question and are debited or credited daily. The securities dealers are entitled to request higher margins the required minimum rates. In the case of all other options transactions the securities dealers can set the margins at their discretion.

Investors must maintain the required margin cover with the securities dealer during the entire life of the contract. A margin shortfall usually results in the liquidation of the position in question by the securities dealer.

Closing out/Settlement

Contracts can be closed out at any time prior to expiry date. Depending on the type of contract and customary practice on the exchange in question, contracts are closed out either by means of an identical counter-transaction or by concluding an offsetting transaction in respect of the obligation, with otherwise identical specifications. In the latter case the delivery and acceptance obligations resulting from the two open contracts cancel each other out.

Obligations arising from the sale of options which are not closed out must always be settled on expiry date. In the case of contracts based on physical assets, settlement usually takes the form of a delivery of the underlying instrument. In the case of contracts based on benchmarks, a corresponding cash consideration is paid in lieu of physical delivery.

Risks

Options transactions can involve major financial risks and should only be entered into by investors who are familiar with this type of transaction, have sufficient liquid resources at their disposal and are able to absorb potential losses.

Options are extremely versatile securities that can be used for many different ways. Investors may use options either for speculation or protection (hedging). Many investors trade in options to speculate on the price movements of an underlying security which can be very risky. On the other hand, investors may use options to protect (or hedge) an open position in an attempt to minimize risk.

Investors should be aware that the buyer of the option has less risk than the writer of the option because if the price of the underlying asset moves against you, you can simply allow the option to lapse. The maximum loss that the buyer can suffer is the option premium plus any other commission and fees. On the other hand, the writer of the option may lose significant amounts, since they have the obligation to buy the underlying no matter how far the market price has moved away from the exercise price. Investors should pay a great attention on the significant losses that they may have when the investor does not own the underlying and sell a call option due to the fact that the market price of the underlying may grow infinitely.

Risks because of changes in the value of the contract/underlying instrument

Generally speaking, if the value of the underlying asset falls, so does the value of your call option. The value of your put option tends to fall if the underlying asset rises in value. The less your option is in the money, the larger the fall in the option’s value. In such cases, value reduction normally accelerates close to the expiration date.

The value of your call option can also drop when the value of the underlying remains unchanged or rises. This can happen as the time value eases or if supply and demand factors are unfavourable. Put options behave in precisely the opposite manner.

You must therefore be prepared for a potential loss in the value of your option, or for it to expire entirely without value. In such a scenario, you risk losing the whole of the premium you paid.

Risks as writer of a covered call option

If, as writer of a call option, you already have a corresponding quantity of the underlying at your disposal, the call option is described as covered. If the current market value of the underlying rises above the strike price, your opportunity to make a profit is lost since you must deliver the underlying to the buyer at the strike price, rather than selling the underlying at the (higher) market value. The underlying assets must be freely available as long as it is possible to exercise the option, i.e. they may not, for example, be blocked by being pledged for other purposes. Otherwise, you are subject to the same risks as when writing an uncovered call option.

Risks as writer of an uncovered call option

If, as writer of a call option, you do not have a corresponding quantity of the underlying at your disposal, the call option is described as uncovered or naked. In the case of options with physical settlement, your potential loss amounts to the price difference between the strike price paid by the buyer and the price you must pay to acquire the underlying assets concerned. Options with cash settlement can incur a loss amounting to the difference between the strike price and the market value of the underlying.

Since the market value of the underlying can move well above the strike price, your potential loss cannot be determined and is theoretically unlimited.

As far as American-style options in particular are concerned, you must also be prepared for the fact that the option may be exercised at a highly unfavourable time when the markets are against you. If you are then obliged to make a physical settlement, it may be very expensive or even impossible to acquire the corresponding underlying assets.

You must be aware that your potential losses can be far greater than the value of the underlying assets you have lodged as collateral (margin cover).

Risks as writer of a put option

As the writer of a put option, you must be prepared for potentially substantial losses if the market value of the underlying falls below the strike price you have to pay the seller. Your potential loss corresponds to the difference between these two values.

As writer of an American-style put option with physical settlement, you are obliged to accept the underlying assets at the strike price, even though it may be difficult or impossible to sell the assets and may well entail substantial losses.

Your potential losses can be far greater than the value of the underlying assets you have lodged as collateral (margin cover).

Difficulty or impossibility of closing out positions

In order to limit excessive price fluctuations, an exchange can fix price limits for certain contracts. The investor must be aware that when the price limit is reached closing out is considerably more difficult or even temporarily impossible. Every investor should therefore make enquiries about any existing price limits before concluding options transactions.

Physical delivery/Cash settlement

Investors are exposed to greater risks with contracts which have to be fulfilled by physical delivery than with those which are fulfilled by cash settlement. In the case of physical delivery the full contract value must be paid, whereas in the case of cash settlement only the difference between the price agreed upon when concluding the contract and the current market value on settlement date must be paid. Investors must therefore have greater liquid resources at their disposal for contracts with physical delivery than for contracts with cash settlement.

Special risks of over-the-counter options transactions and transactions with warrants and stock options

As a rule, the market for standardized OTC options transactions and for transactions in warrants and stock options listed on an exchange is transparent and liquid. Closing-out is therefore usually possible without any significant problems.

By contrast, there is no market as such for OTC options transactions with individual contract specifications and for transactions in warrants and stock options which are not listed on an exchange. Closing out is therefore only possible if counterparty is found who is prepared to conclude an offsetting contract.

Combined transactions

Combined transactions are understood to mean the conclusion of two or more options transactions on the same underlying instrument. In such cases the options differ at least in respect of type (call or put), quantity, striking price, expiry date and/or the position taken (long, short).

Due to the diversity of possible combinations, the risks arising in a specific instance cannot be dealt with in detail within the scope of this notice. They can also be altered substantially by closing out individual elements of a combined transaction. Before concluding a combined transaction, investors should therefore make detailed enquiries about its specific risks.

«Exotic» options

Unlike “plain vanilla” put and call options exotic options (average rate options, currency-protected options, path-dependent options, complex basket options, compound options etc) are subject to additional conditions or agreements. They feature structures which cannot be created by any combinations of standard options alone or together with underlying instruments. «Exotic» options occur both as OTC options and also in the form of warrants.

The virtually unlimited possibilities for structuring «exotic» options mean that the risks arising in individual instances cannot be described within the scope of this notice. Investors should therefore seek detailed information about the risks involved before purchasing or selling instruments of this nature.

In addition to the above risks dealing in options involve also the following risks:

Calls (standardized purchase options):

- For the purchaser: credit risk, inflation risk, market risk, country risk, liquidity risk, exchange risk, interest-rate risk (indirect).

- For the writer (in uncovered trading): credit risk, high market risk due to leverage, country risk, liquidity risk, exchange risk, interest-rate risk (indirect), risk of having to sell the instruments underlying the call at less than the current market value.

Puts (standardized selling options):

- For the purchaser: credit risk, inflation risk, market risk, country risk, liquidity risk, exchange risk, interest-rate risk (indirect).

- For the writer (in uncovered trading): credit risk, high market risk due to leverage, country risk, liquidity risk, exchange risk, interest-rate risk (indirect), risk of having to purchase the instruments underlying the put at more than the current market value.