European Banks Face Capital Hit From Second-Quarter Bond Selloff

The bond market selloff in the second quarter probably dented the capital defenses of many European banks, with lenders in Italy and Spain hit hardest.

The extent of the damage will be disclosed when banks report earnings starting this week. It probably won’t be so much as to force lenders to sell shares, analysts at brokerages including Nomura Holdings Inc., Deutsche Bank AG and Citigroup Inc. agreed.

“Following the second-quarter performance of peripheral bonds, a key focus this quarter will be the potential impact from sovereign exposure,” analysts at Nomura, including Jaime Hernandez and Jon Peace, wrote in a note July 20. “Spillover to Spain and Italy is the key concern we would watch for given the much greater holdings of these bonds, primarily by domestic banks.”

The upheaval in the bond market was a setback for southern European banks. Their earnings are already under pressure from low interest rates, and investors are punishing lenders with lower capital levels. Margins on loans at Italian and Spanish banks narrowed the most among European countries in the second quarter, according to the European Central Bank.

The securities hit most by the rout are probably longer-term European government bonds that are available for sale, as opposed to assets that have to be held to maturity. Price declines for these assets don’t hurt earnings but they do squeeze capital under tougher post-crisis rules to ensure bank losses don’t threaten the wider economy.

Italy’s two biggest banks, Intesa Sanpaolo SpA and UniCredit SpA, both incurred unrealized losses of more than 1 billion euros ($1.1 billion) on these assets, as did Banca Monte dei Paschi di Siena SpA, JPMorgan Chase & Co. analysts led by Kian Abouhossein estimated in a July 2 note. That would leave Monte Paschi with a common equity Tier 1 ratio, a measure of lost-absorbing ability, of 8.5 percent, closer to the regulatory minimum of 8 percent — this after a cash call in April. It began the quarter with a CET1 ratio of 10.2 percent.

Italian banks stepped up purchases of the country’s government bonds in the first quarter, riding a rally sparked by the advent of the ECB’s huge bond-buying program in March. Italian lenders were holding a near record-high 415.5 billion euros of their country’s sovereign debt at the end of April.

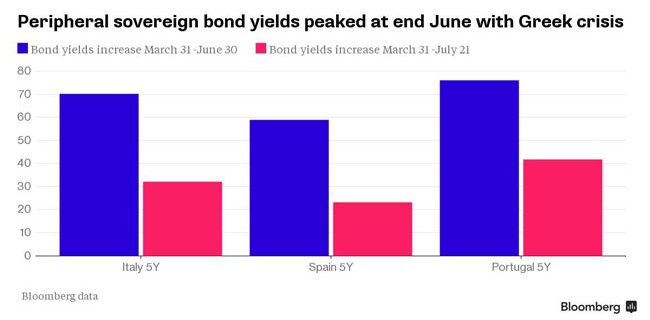

The mood changed in May, when investors balked at record-low borrowing costs after early signs of a pickup in inflation, which erodes the value of bonds over time. Yields on Italian and Spanish benchmark 10-year bonds spiked again in June during the showdown between Greece and its creditors and amid speculation of an increase in U.S. borrowing costs. Yields and prices move in opposition directions.

In Spain, CaixaBank SA lost 328 million euros, leaving it with a CET1 of 11.3 percent, down from 11.6 percent, according to the JPMorgan analysts, who assumed the full application of Basel III rules, which are still being phased in. Santander SA would have a capital ratio of 9.9 percent, down from 10 percent after 630 million euros in losses on its sovereign bonds, the report says.

Other Spanish banks also probably saw losses on government debt, but they currently benefit from an exemption to rules requiring the markdown in capital. On average, yields on European five-year sovereign bonds rose 38 basis points, more than a third of a percentage point, during the quarter, translating to an average capital hit of 22 basis points for banks that do have to count unrealized losses.

Some of those losses have already been erased. Bond yields fell this month after Greece agreed to European terms for further negotiations on financial aid for the country. The hit may have been mitigated by hedging and developments like the sale a stake in CaixaBank’s online subsidiary Boursorama to Societe Generale SA.

Source: Bloomberg – European Banks Face Capital Hit From Second-Quarter Bond Selloff

Related Posts

ECB keeps banks on tight leash for health check results

ECB keeps banks on tight leash for health check results ECB: Greek banks won’t need even more recapitalisation

ECB: Greek banks won’t need even more recapitalisation Greece to get 6 billion euros in bridge loans if no agreement at Eurogroup

Greece to get 6 billion euros in bridge loans if no agreement at Eurogroup Greece debt crisis: EU leaders gather for critical summit

Greece debt crisis: EU leaders gather for critical summit Draghi’s dilemma: ECB’s five options to boost the eurozone economy

Draghi’s dilemma: ECB’s five options to boost the eurozone economy