US Stock Market Regained The Lead In Last Week’s Rally

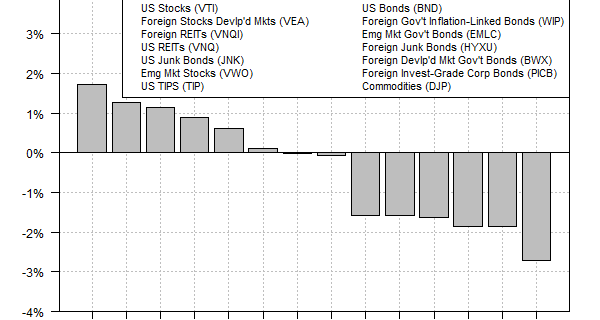

US stocks reclaimed the top spot in last week’s performance race for the major assets classes, based on a set of proxy ETFs. The Vanguard Total Stock Market ETF (VTI) gained 1.7% for the five trading days through Oct. 23, the fourth straight weekly rise—the longest winning streak in a year. Otherwise, the week just passed was mixed for the major asset classes, with broadly defined commodities—iPath Bloomberg Commodity (DJP)—leading the losers with a 2.7% loss—the biggest weekly slide since August.

US stocks reclaimed the top spot in last week’s performance race for the major assets classes, based on a set of proxy ETFs. The Vanguard Total Stock Market ETF (VTI) gained 1.7% for the five trading days through Oct. 23, the fourth straight weekly rise—the longest winning streak in a year. Otherwise, the week just passed was mixed for the major asset classes, with broadly defined commodities—iPath Bloomberg Commodity (DJP)—leading the losers with a 2.7% loss—the biggest weekly slide since August.

Most of last week’s gains were in stocks, although high-yield bonds inched higher too. The prospects of more (or ongoing) monetary stimulus was a factor in bidding risky asset prices up. The crowd decided that the Federal Reserve would continue to delay an interest rate hike, perhaps into 2016. Meanwhile, the Bank of China on Friday announced a rate cut in an effort to juice its economy after a run of economic reports that reflect slowing growth.

In addition, the European Central Bank (ECB) last week hinted that it would roll out additional stimulus efforts next month to bolster a softer trend across the Eurozone. “The risks to the euro area growth outlook remain on the downside, reflecting in particular the heightened uncertainties regarding developments in

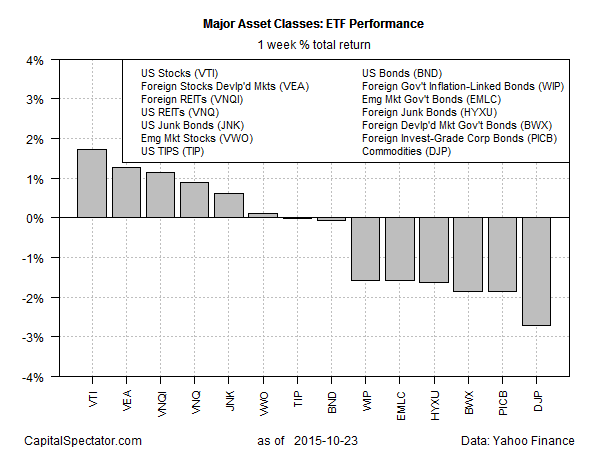

The latest weekly rally in US stocks is once again providing a rosy glow to the trailing 1-year return. VTI is ahead by 7.9% for the year through Oct. 23—second only to US real estate investment trusts–Vanguard REIT (VNQ), which is up 8.9% in annual terms through last Friday.

“The main factor behind the global ebullience [for equities],” notes Andrew Adams of Raymond James, “appears to be a collective confidence that the low-interest rate environment is going to continue for the foreseeable future.”

But that’s also a clue for thinking that economic growth will be weaker generally. The risk-on trade for equities, in other words, may be less compelling than last week’s pop in stocks suggests.

The markets will continue to walk a fine line. Slow growth will hang over the world economy for the foreseeable future. But that means that the odds will stay low for squeezing monetary policy, in the US or anywhere else. Deciding if this amounts to a net plus for risky assets will remain a tough needle to thread. Perhaps, then, it’s reasonable to assume that animal spirits will wax and wane for the near term with muted price trends overall. The economic outlook probably isn’t as dire as the pessimists anticipate, but breaking free of moderate (and in some cases tepid) growth isn’t going to be easy.

As a result, the latest rally in stocks looks less like the start of a new sustainable uptrend vs. a bounce back from the a wave of pessimism that went a bit too far. Until the macro backdrop offers more convincing support, the markets may be destined to suffer a fair amount of churning as the crowd struggles to find a narrative in the noise.

By James Picerno, http://www.capitalspectator.com/

Find more: Contributing Authors