Draghi Defines His Era With Stimulus Measures Locked Into Next Decade

-

Lending program can lock in ultra-low rates until next decade

-

ECB action provides rebuttal to doubts over central bank power

Whether Mario Draghi’s latest barrage of stimulus works or not, the European Central Bank president made one thing clear on Thursday: he won’t be the one to clean up afterward.

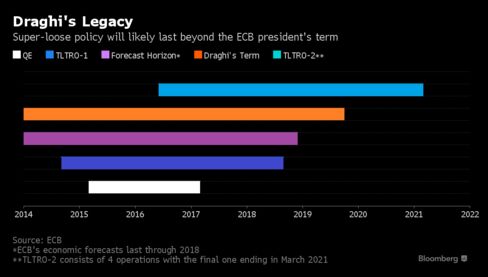

Instead, ultra-low interest rates that might even pay banks to receive loans are now potentially locked in until after the Italian retires in 2019. The ECB’s new measures have just entrenched policies designed for crisis times into the next decade.

In the face of a global debate on whether monetary policy has lost its effectiveness and is even planting the seeds of the next crisis, the ECB has delivered a solid defense of the right and power of central banks to boost growth and inflation at will. The best that can be said for euro-area fiscal policy is that it’s not hampering the recovery, so Draghi has underlined that he won’t wait for others to act.

“It’s hard to see what would happen with the euro-zone economy without the ECB being there, and obviously they could do more of the same and then even more of the same,” said Carsten Brzeski, chief economist at ING DiBa in Frankfurt. “The situation could be that just as Draghi became governor to reverse Trichet’s rate increase, so it’ll be up to Draghi’s successor to unwind all the unconventional policies and rate cuts.”

Thursday’s meeting in fact helped shape the entire span of Draghi’s term in office, reaching from his immediate reversal of his predecessor’s two 2011 rate hikes after he took charge in November that year, through the torturous debate leading up to quantitative easing, and now embedding bank-friendly credit policies until beyond the end.

The president announced cuts to all three of the ECB’s rates, bringing the deposit rate to minus 0.4 percent, and a 20 billion-euro ($22 billion) expansion of quantitative easing that for the first time opens the door to purchases of corporate bonds. On top of that, he announced a new four-year loan program that potentially allows banks to be remunerated for taking the ECB’s money if they expand credit to the real economy, in a quartet of operations stretching to 2021.

Draghi’s policy arc has been in defiance of warnings by monetary conservatives, including those in Germany’s Bundesbank since the beginning of his term, up to more recent calls by the Group of 20 nations to shift the burden of growth generation away from monetary policy and toward structural policies or more government investment.

Instead, Draghi sounded resigned when asked about euro-area fiscal policy. That domain spans countries including Spain, France and Italy that are close to their legal deficit limits, and nations that can afford to spend more — read Germany — that have promised voters they won’t do so.

“The measured driver of the economy and the recovery basically remains our monetary policy,” he said.

That leaves the ECB as the guarantor of monetary and financial conditions in the euro area until political reality changes — a role Draghi wasn’t willing to admit at his news conference.

He also argued that there’s no mechanical link between the 4-year loan program and the benchmark rate, meaning official rates could rise after the central bank’s current bond-purchase scheme finishes in 2017 — albeit in his words “well past the horizon of our net asset purchases.” Even then, the ECB will have built up a stock of assets that may take years to unload from its balance sheet.

Thursday’s package does push out the period of easy monetary policy and helps banks plan over the long term. Combined with his excursion into new, riskier asset classes, Draghi is showing he has plenty of ammunition left, according to Marchel Alexandrovich, senior European economist at Jefferies International Ltd in London.

“We are optimistic that it will work,” Alexandrovich said. “But there’s a consistent struggle in the mind of the markets that we’re looking at a new normal of lower growth and lower inflation, and the future isn’t going to be like what we were used to before.”

Source: Bloomberg

Related Posts

Draghi and Yellen leave EUR/USD in range

Draghi and Yellen leave EUR/USD in range Draghi sends the Euro Lower on Thursday, Seen Paring Losses Mid-Day

Draghi sends the Euro Lower on Thursday, Seen Paring Losses Mid-Day The European Central Bank keeps key interest rates at historic lows

The European Central Bank keeps key interest rates at historic lows Bank of Japan:Statement on Monetary Policy

Bank of Japan:Statement on Monetary Policy TICKING TIME-BOMB: Greece set to run out of cash by MAY pushing Europe into ANOTHER crisis

TICKING TIME-BOMB: Greece set to run out of cash by MAY pushing Europe into ANOTHER crisis