BofAML upgrade forecasts for British Pound v Euro and Dollar

Bank of America Merrill Lynch (BofAML) have told clients they are now confident enough on Pound Sterling to raise their forecast profile.

Analysts had been expecting one final dip in the UK currency ahead of a more sustained recovery, but it appears that such slippage is unlikely now that the UK is headed for a general election which is expected to hand Prime Minister May a stronger hand in upcoming Brexit negotiations.

“In the immediate aftermath of the election announcement, we argued that the announcement was a game changer for GBP as the downside risks had markedly diminished. Up until then, we had expected one final dip in GBP/USD at the commencement of Brexit negotiations potentially providing a buying opportunity for a medium-term recovery due to Sterling’s undervaluation relative to its medium-term fundamental drivers,” says analyst Kamal Sharma at Bank of America Merrill Lynch in London.

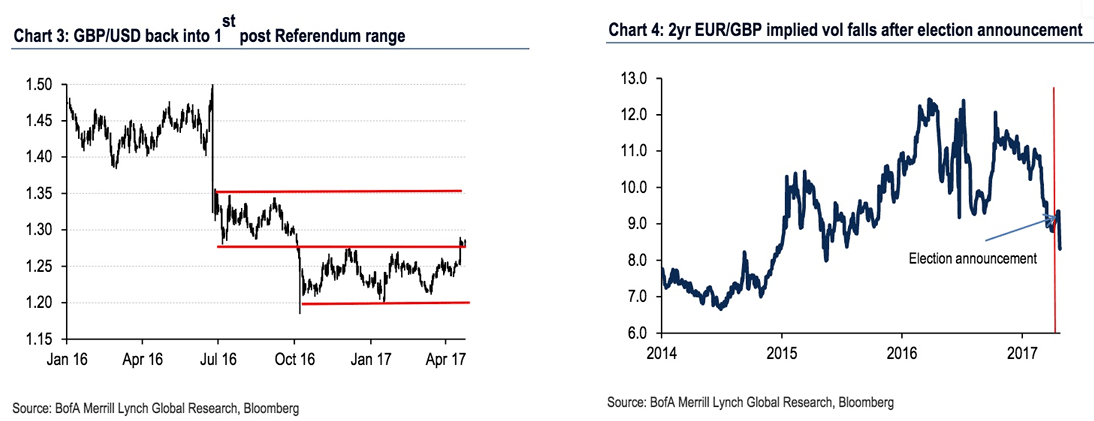

Looking at Sterling’s prospects over the next few weeks, Sharma explains the currency still faces some near-term headwinds which should keep GBP/USD capped below $1.30 for the time being.

This is an important level as shown in the below:

Some Near-term Challenges Remain

But, there are some risks to be aware of in the next one to four weeks.

“As much as historically April seasonality has been a consistent positive for GBP/USD, May has been as negative for GBP/USD since 2010,” says Sharma.

We warned at the start of April that it was a month that tends to smile on Sterling, and so it was.

Not only did the Pound better the US Dollar but it better the next twenty major currencies too.

Seasonality tends to favour downside in May albeit less than the average upside of 2.2% favoured in April, which also has a seasonal bias.

“We concede that the observed seasonality is not strong in May as it is in April (+2.2% appreciation on average in April versus -0.81% decline in May since 2005) but GBP/USD has consistently fallen in May since 2010,” said Sharma.

Also note how Sterling underperforms ahead of UK General Elections.

“GBP/USD tends to underperform into and following General Elections, whilst the prospect of large majorities has not immediately translated into a higher cable. We think there is a risk that markets could buy the large majority ‘consensus’, but sell the fact,” says Sharma.

It is worth pointing out that the outcome of the June 8 election is not as uncertain as was the case in the last two General Elections, so we would argue there is the chance that this well-flagged event might not impact Sterling as has been the case in the past.

Recent Upside Momentum Might Fade

Sterling may find it more difficult to maintain upside momentum, however, as the days when the majority of investors were short the currency have passed and GBP positioning in the futures market as measured by CFTC data, for example, is now much more balanced.

This means there is less risk of a short-covering rally giving the Pound an upside boost as most of the short-sellers have already liquidated their positions.

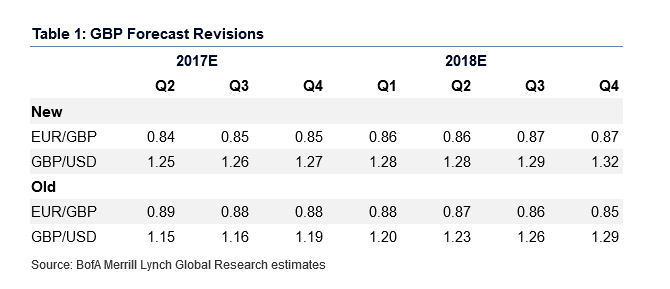

Options market pricing is also showing less risk of downside. Options are used by many investors to hedge their deals.

“Our positioning scorecard shows that risk reversals have moved to significantly price out GBP downside risks,” says Sharma.

Nevertheless, although, “pessimism towards GBP may have been priced out of the options market,” investors may not, “yet be ready to translate this into outright bullishness,” says Sharma.

There is also evidence that GBP is regaining its previous role as a risk-on currency and Sharma notes how it is now correlating quite closely with the S&P 500, the original barometer for global risk appetite.

But, Sterling’s New Equilibrium will be Lower

Although the BofAML analyst expects GBP/USD to recover, he does not see it recovering all the way to pre-referendum equilibrium levels.

“A slowing domestic economy tempers prospects of sustained upside,” says Sharma.

Whilst he highlights the current account deficit as the currency’s ‘Achilles Heel,’ the latest balance of payments data reveal foreign direct investment (FDI) inflows increasing.

This is likely due to the weaker Pound making UK assets attractive to foreign investors and this should support improvement in the Current Account and Sterling “towards equilibrium again”.

The flow of investor capital into the country offsets the outflows arising from the UK’s heavy reliance on imports, and this offsetting flow supports the currency.

“Investor confidence remains crucial for GBP and the current account deficit remains its Achilles Heel. Nonetheless, balance of payments reveals that the UK recorded very strong FDI inflows in 2016 against the backdrop of currency weakness and a resilient economy,” says Sharma.

Q4 2016 saw the UK post its largest quarterly net inflow (£110bn) of FDI since Q1 2014.

In a year which was meant to bring great political and economic uncertainty, 2016 net FDI inflows hit nearly £200bn, over 2.5 times the amount of net inflows in 2015, and this has certainly bouyed Sterling as 2016 FDI inflows into the UK were nearly six times larger than in 2015.

“A combination of a weak currency and resilient UK growth has undoubtedly been the main drivers for this surge in FDI inflows,” notes Sharma.

Sterling’s progress is therefore likely to be heavily impacted by investor confidence going forward, which so far has remained remarkably resilient.

“GBP will likely trade at a structurally lower equilibrium level and GBP/USD is unlikely to regain its pre-Referendum range. A slowing domestic economy tempers prospects of sustained upside,” says the analyst.

Upgraded Forecasts

Bank of America Merrill Lynch Global Research lower their EUR/GBP profile as they raise their GBP/USD profile.

Their longer-term (multi-month) picture is more constructive and we find it follows a ‘dip first, recovery later’ pattern that other analysts have suggested.

“The announcement of an 8th June General Election was a game changing event for GBP. We have consequently revised our GBP forecasts which mainly impact the front-end of the profile, no longer expecting the one final dip. Our end-2018 GBP/USD takes us closer to our estimates for fair value than previously,” says Sharma.

So while the election itself appears as something that might offer negativity for Sterling, the longer-term implications of a stable Conservative majority government is seen as a positive underpinning for the currency’s trajectory.

It is noted that GBP/USD was 10% below fair value but is currently rapidly making up ground.

Previously the analyst had forecast a final dip to 1.15 but he has now revised that up to something much ‘shallower’.

The EUR/GBP exchange rate is forecast at 0.85 in the third quarter of 2017 where it should remain into year-end.

The Euro is forecast to push the Pound to 0.86 in the first quarter of 2018 where it should stay until the third quarter where it will rise to 0.87.

This translates into a Pound to Euro exchange rate of 1.1765 and 1.1628 respectively.

While spot GBP/EUR is currently above these levels note that they are upgrades on previously-held forecasts.

For instance the exchange rate was previously forecast to end 2017 at 1.1364.

Therefore the message is the downside risks have diminished in the eyes of BofAML.

Source: PoundSterling

Related Posts

British Pound vs Dollar, Euro: The Only Way is Up in 2017 Forecasts Nordea

British Pound vs Dollar, Euro: The Only Way is Up in 2017 Forecasts Nordea Pound wobbly, yen edges higher on mounting Brexit worries

Pound wobbly, yen edges higher on mounting Brexit worries The Pound to Euro Exchange Rate in Sudden Reversal as US Dollar Slides

The Pound to Euro Exchange Rate in Sudden Reversal as US Dollar Slides Pound logs biggest quarterly drop since the financial crisis

Pound logs biggest quarterly drop since the financial crisis Massive Demand for UK Gilts Spurs GBP/USD Higher

Massive Demand for UK Gilts Spurs GBP/USD Higher