U.S. accountants’ optimism returns to pre-recession levels

Not since 2007 have U.S. accountants in industry felt as optimistic about the future of their companies and the state of the domestic economy as they do now.

While concerns about regulatory requirements linger, and some companies remain hesitant to deploy cash or hire, those potential obstacles can’t stem the rising tide of optimism regarding U.S. businesses’ next 12 months. That’s what the numbers show in the third-quarter Business & Industry Economic Outlook Survey, released Thursday by the AICPA.

Since the third quarter of 2012, optimism about the U.S. economy has gone from 22% to 52%. Optimism about finance professionals’ own companies has risen from 44% to 65% in that span.

Across sectors, companies are optimistic that they will grow revenue, profits, and head count in the next 12 months. Revenue is expected to rise 4.4% in the coming 12 months; profit is projected to rise 3.6%; and head count is projected to rise 1.8%. Each indicator reached its highest level since 2007.

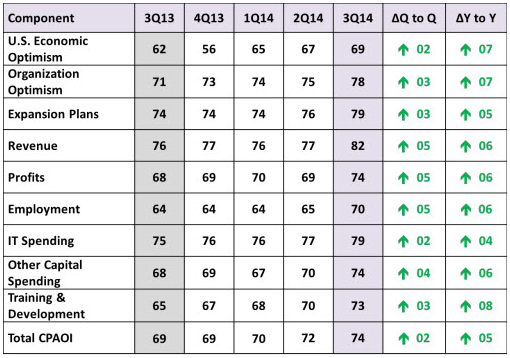

The survey measures the sentiment of more than 1,100 high-ranking finance professionals—mainly CEOs, CFOs, and controllers—in nine areas: U.S. economic optimism, organization optimism, expansion plans, revenue, profits, employment, IT spending, training and development, and other capital spending.

Those components make up the CPA Outlook Index, which hit 74, the highest mark since the first quarter of 2007. An index rating above 50 indicates a positive outlook.

All nine components in the index have increased by at least four points in the past year, led by an eight-point rise in planned spending for training and development.

One measure of optimism in the United States is increased shipping imports, said Valerie Rainey, CPA, CGMA, the CFO at INTTRA, a global e-commerce provider for the shipping industry. The company publishes a monthly ocean-freight index jointly with Cass Information Systems, and the most recent one, from July, shows year-over-year growth of 5.8% for U.S. imports and month-over-month growth of 15.4%. The index measure for imports is the highest since the survey began in January 2010.

“When that happens, what are [companies] doing? They’re replenishing their inventory,” said Rainey, vice chair of the AICPA Business & Industry Executive Committee.

Regulation still atop list of challenges

Respondents were asked their top challenges. The top challenges cited, in order, were regulatory requirements and changes, domestic economic conditions, availability of skilled personnel, and employee and benefits costs. Organizations project health care costs to rise 6.6% in the coming year.

David Citarelli, CPA, feels the sting of increased costs. Citarelli, the CFO of McDevitt Trucks, a seller of heavy-duty trucks with five dealerships in Massachusetts, New Hampshire, and Vermont, said an early projection for health care costs in the coming year showed a 17% increase. And factory-mandated training, part of the company’s franchise agreements, eats up much of McDevitt’s training budget.

Citarelli is mildly optimistic about his company’s prospects, even though he doesn’t project sales of new heavy-duty trucks to rise. Consumers continue to hold on to vehicles longer than they did in the past. “The service-and-parts business will continue to be reasonably stable,” said Citarelli, who added that his company doesn’t expect to add staff in the coming year.

Overall, according to the survey, 20% of companies plan to hire staff, up from 15% who planned to hire a year ago. Just more than half of organizations (51%) say they have the right number of employees, and 18% say they have too few workers but are hesitant to add more. A year ago, 53% had the right number, and 19% were hesitant to hire.

Other highlights from the survey:

- The Northeast and Midwest regions showed strong gains in company optimism. Northeast companies’ optimism rose to 68% from 52% a year ago. Midwest companies’ optimism rose to 66% from 55% a year ago. Optimism in the South (63%) and West (62%) rose less dramatically.

- Companies remain hesitant to deploy cash. The number of respondents indicating they had about the right amount of liquidity rose to 47% from 42% a year ago. Overall, fewer have less cash than they need compared with the previous year. Nineteen percent have more than they need but are reluctant to deploy it, and 15% have more than they need and plan to deploy it. Those numbers are down from 21% and 16%, respectively, a year ago.

- Optimism in the professional-services sector rose to 76% from 54% a year ago, including a 12-point gain from the previous quarter. Manufacturing has risen 16 points in the past year (56% to 72%), and the construction, real estate, and health care sectors also have made gains of 10 or more percentage points in the past year. Optimism in technology has dropped two consecutive quarters and stands at 58%, two points higher than a year ago.

- Expectations for training spending have risen four consecutive quarters, and projections for other capital spending have increased two consecutive quarters.

The CPAOI

Each component of the CPAOI is calculated by taking the percentage of respondents who indicated that their opinion or expectation for the metric is positive or increasing, and adding to that half of the percentage of respondents indicating a neutral or no-change response. A reading above 50 indicates a generally positive outlook with increasing activity. A reading below 50 indicates a generally negative outlook with decreasing activity.

For example, if 60% of respondents indicate an optimistic or very optimistic view and 20% express a neutral view, the calculation of the component indicator would be 70 (60% + [0.5 × 20%]).

CPA Outlook Index Component

Source: JoA

Related Posts

When Should You Give Investors Their Money Back?

When Should You Give Investors Their Money Back? No Company Too Small to Pursue Finance Operations Excellence

No Company Too Small to Pursue Finance Operations Excellence Why accountants are dissatisfied with their job?

Why accountants are dissatisfied with their job? Big four among others to join together to enable more apprenticeships

Big four among others to join together to enable more apprenticeships Indirect tax rates continue to soar across the globe as governments devise new levies

Indirect tax rates continue to soar across the globe as governments devise new levies