Fitch: Steep Emerging-Market FX Reserve Falls Likely to Continuee

Global EM FX reserves have fallen by USD524bn since June 2014, surpassing the drop in 2008-2009, and further declines are probable.

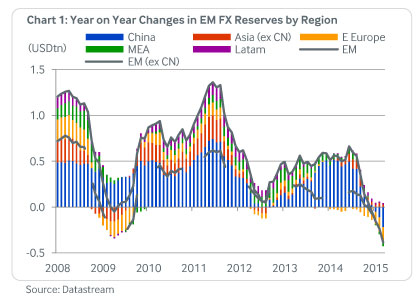

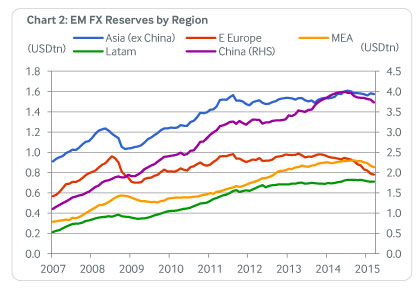

Emerging-market (EM) official foreign exchange (FX) reserves have been falling steadily by an average of USD58bn a month since reaching an all-time high of USD8.17trn in June 2014. This has mainly been due to reductions in China and Russia, but is accentuated by declines elsewhere. Total reserves have also been falling year on year from December 2014, with the cumulative yearly decline accelerating to USD385bn in March 2015 (USD167bn excluding China; see Chart 1).

Typically, reserve reductions indicate balance-of-payments pressures and/or central bank interventions in currency markets to dampen exchange rate depreciations. Greater exchange-rate flexibility across EMs and previous reserve accumulations alleviate most immediate concerns, including in China and Russia, but much depends on the direction of commodity prices and global market reactions to the eventual increase in US policy rates.

September 2008 to April 2009 was the only other period in which EM reserves have fallen significantly since the 1997 Asian crisis. Then, the recovery was supported by rapid accumulation in China: EM reserves reached new highs only three months later, in July 2009 (December 2009 excluding China). But the present decline is different in several respects.

By March 2015, EM reserves were down by USD524bn (USD260bn excluding China) from the June 2014 peak. This is already much larger than the USD358bn (USD386bn excluding China) reduction in 2008-2009.

This time, the decline includes China, unlike in 2008-2009 when Chinese reserves increased steadily. The 2008-2009 episode was led by emerging Europe and emerging Asia excluding China.

The current reduction was not preceded by a run-up in reserves. In 2008, and again between 2009 and 2011, all EM regions experienced strong increases in reserves. In contrast, from 2012 to mid-2014 EM reserves were largely flat outside China and the Middle East and Africa.

Partial data for April suggest the decline in EM reserves is continuing, and remains widespread. There are few reasons to expect an imminent change to recent trends in China and Russia. Other EMs are still facing weak commodity prices – although with some stabilisation in recent months – and the prospect of further adjustments in global capital flows when the US eventually tightens monetary policy.

Common Causes: Valuation Changes, Commodity Prices, and Capital Outflows

Of 29 EMs surveyed by Fitch, the biggest percentage reductions in FX reserves since the beginning of 2014 have been in Nigeria, Russia, Malaysia, Romania, South Africa, and Hungary. In all countries, a degree of valuation change (specifically, a stronger US dollar) is likely to account for some of the reduction in the dollar value of reserves. This is likely to be most pronounced in Romania and Hungary, where other external sector issues can largely be set aside, and possibly a notable factor in Russia and South Africa.

Two further common causes of the reduction in EM FX reserves are the falls in commodity prices that began in 2014, leading to trade and current account deteriorations in commodity exporters, and an acceleration of capital outflows for some countries.

Malaysia is affected by lower commodity prices, and is therefore running a smaller current account surplus, but it was a pickup in capital outflows – especially portfolio flows and “other investment”, which is typically borrowing – that made the difference in recent quarters. Russia is also running a consistent current account surplus (except for a small deficit in 3Q14). Again, it is capital outflows that have driven reserves lower, in this case due to the effects of economic and financial sanctions imposed by Western governments, requiring net repayments of Russian external debt and contributing to significant capital flight.

High-frequency data in Nigeria are less readily available than for other EMs, but we believe that it too has suffered a significant current account deterioration due to lower oil prices and large capital outflows. South Africa’s current account deficit has widened substantially since 2011 with the disappearance of the trade surplus, while capital inflows have increased (mostly “other investment” in recent quarters) at a slightly slower rate.

Source: FitchRatings – Steep Emerging-Market FX Reserve Falls Likely to Continue