The Fed Talks And The Market Tanks. That’s Different

Normally there’s a distinct pattern to the impact of Federal Reserve statements on the financial markets. The tone of equities trading in particular starts to improve as the moment of the announcement approaches; the words turn out to be blandly positive, full of promises of easy money and upbeat forecasts; and share prices soar for a day or two. It’s been thus for most of the past six years, leading large numbers of new investors and recently-minted analysts and traders to see the Fed as a modern version of Plato’s philosopher king, wielding absolute power to achieve perfect justice in the form of rising asset prices.

Normally there’s a distinct pattern to the impact of Federal Reserve statements on the financial markets. The tone of equities trading in particular starts to improve as the moment of the announcement approaches; the words turn out to be blandly positive, full of promises of easy money and upbeat forecasts; and share prices soar for a day or two. It’s been thus for most of the past six years, leading large numbers of new investors and recently-minted analysts and traders to see the Fed as a modern version of Plato’s philosopher king, wielding absolute power to achieve perfect justice in the form of rising asset prices.

So it must have been a shock yesterday when the Fed released the minutes of its last meeting — which were full of the usual bland equivocations aimed mostly at not upsetting anyone, though with the recently added promise of a tiny rate increase one of these days — and the markets tanked. As of this writing (noon-ish on Thursday) US equities are down over 1% and the S&P 500 has turned negative for the year. Bond yields are falling, gold and silver are rocking, and the sense of fear, confusion, and betrayal is palpable.

What happened? What inevitably had to. Liquidity-driven markets love low interest rates and massive money creation. But those things cause imbalances that eventually become self-negating. The bang for each dollar of newly-printed or borrowed currency falls to zero and then turns negative.

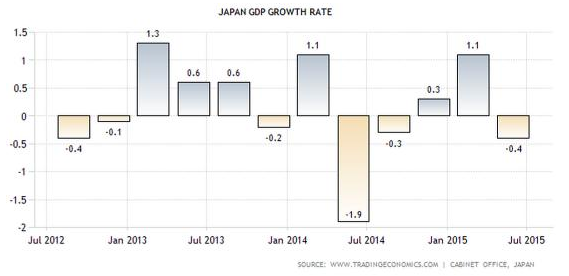

That’s happening now as the major economies continue to borrow but can’t seem to turn the proceeds into measurable growth. Japan, for instance, is running epic deficits and monetizing the whole thing, but over the past five quarters its economy has gotten smaller. Which is another way of saying its ratio of debt to GDP is soaring at an accelerating rate.

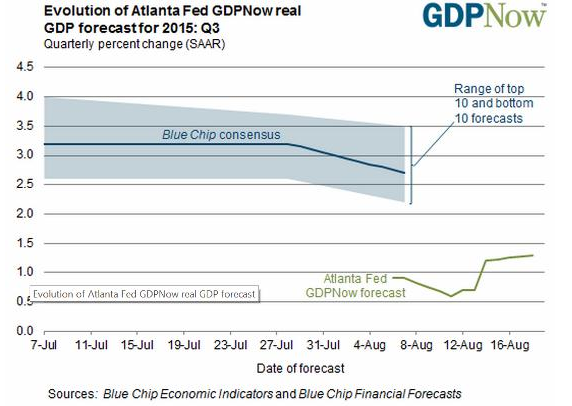

The Atlanta Fed, which has been highly-accurate lately in its near-term predictions, now has the US growing at a rate of less than 1.5% in the third quarter, far below the 3% needed to stop the growth in debt/GDP.

Europe’s growth is less than 1%, with most of that coming from Germany. And China, well, it claims to be growing but most of the world now suspects it’s in recession — if that’s not too bland a word for the crisis unfolding there.

So, back to the Fed. The markets have been buying the promise that adult supervision and superior judgment on the part of the monetary authorities would produce steady growth and continued easy money. But now a bit of doubt has begun to creep in. What if these guys are not in fact omnipotent and all-seeing? What if the trends they’ve engendered are finite? And what if they don’t have a plan for avoiding the brick wall that seems to be blocking this smooth stretch of highway? What indeed?

By John Rubino, http://dollarcollapse.com/

Find more: Contributing Authors