Deloitte’s latest survey results: Audit of the Future

Audits play a fundamental role in the capital market system, and Deloitte’s latest survey of more than 250 financial statement preparers, audit committee members and financial statement users reveals a shared sense that the traditional audit needs to evolve. How should the audit profession begin to address these evolving demands? See the latest survey results below to get a glimpse of the current—and future—states of the audit below.

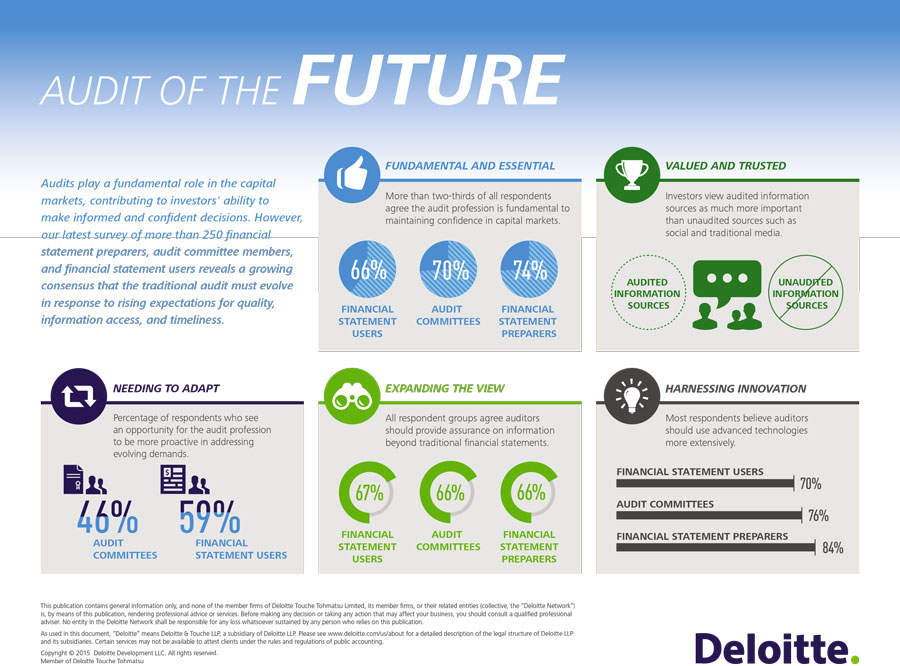

Source: Deloitte

Investors, Audit Committees Want Auditors to Expand Scope of Assurance: Deloitte Survey

More than half (59%) of financial statement users seek more from the audit profession to address growing demands of the capital markets, according to Audit of the Future, a survey from Deloitte & Touche LLP representing the opinions of 250 financial statement users including investors, audit committee members and financial statement preparers.

“Many investors are looking for broader and deeper insights that can help them make smarter, more informed decisions,” notes Joe Ucuzoglu, chairman and CEO of Deloitte & Touche LLP, and leader of Deloitte’s audit practice. “The audit profession as a whole will be looked at to expand outside the domain of the historical financial statements.”

More than two-thirds of all survey respondents agree that the audit profession is fundamental to maintaining confidence in capital markets by providing assurance that financial statements are free of material misstatements and companies’ systems of internal control over financial reporting operate effectively.

“The investing public is looking to a trusted source in an increasingly complex and challenging global business environment. This survey clearly indicates traditional audits must evolve to meet the needs of the capital markets and today’s investors,” Mr. Ucuzoglu adds.

The survey results also highlight that financial statement users have limited ways to fully understand the audit results and what auditors do in fulfilling their professional responsibilities, other than what is written in the auditors’ reports.

Further, 46% of audit committee members would like the audit profession to be more proactive in addressing evolving demands. All respondent groups strongly agree that auditors should provide assurance on information beyond traditional financial statements, such as earnings releases, investor presentations and risk factors, with at least two-thirds of each survey respondent group feeling that way. In addition, investors view audited information sources as more important than unaudited sources, such as social and traditional media, according to the survey.

“More direct engagement between the audit profession and financial statement users can allow for a better understanding of user needs,” observes Mr. Ucuzoglu.

Specifically, Mr. Ucuzoglu says that auditors need to be open to reporting on the most important business metrics that move markets, such as key performance indicators, industry metrics and non-GAAP measures, all of which are becoming increasingly relevant to investment decisions.

Technology-driven Innovation

More than three-quarters of audit committee members (76%) and financial statement preparers (84%) surveyed believe there are significant benefits to auditors using advanced technologies. In addition, virtually all survey respondents strongly agree that more advanced technologies should be used in the execution of an audit. However, while 70% of audit committee members and financial statement preparers say that the audit profession’s adoption of innovative technology and process improvements keeps pace with their industry, other financial statement users are less convinced, with only 45% of those respondents agreeing.

“The business environment is constantly shifting, spurred by technology innovations and evolving business models,” says Mr. Ucuzoglu. “To deliver the most value, the audit profession must rapidly transform itself. This will require significant investments, and a mindset that is bolder than the public accounting profession has historically been known for.”