BaFin and the SEC: An international comparison of supervisory practice

The Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht – BaFin) is often compared to the U.S. Securities and Exchange Commission (SEC) in the media and by the public. The SEC is frequently perceived as the more powerful authority, in particular due to the high penalties imposed and the large settlement amounts agreed by it.

The differing perceptions of BaFin and the SEC stem from discrepancies in jurisdiction and regulatory powers of the two authorities as well as between the US and German, or European, legal systems. However, the size of the penalties imposed must not cause the wrong conclusions. An objective analysis demonstrates that BaFin’s supervisory practice has an effect on the companies it supervises similar to the SEC’s on US capital market participants. In addition, new EU financial market regulation will expand BaFin’s powers in the coming months, in particular the implementation of the second Markets in Financial Instruments Directive (MiFID II), the revised Transparency Directive and of parts of the Market Abuse Regulation.

Jurisdiction

An important difference between BaFin and the SEC is their areas of responsibility. The model of a “universal supervisor”, as embodied by BaFin, does not exist in the US. While BaFin unifies securities, banking and insurance supervision under its roof, the SEC is not responsible for supervising banks or insurance undertakings. It supervises, in particular, brokers, investment advisers, clearing houses and stock exchanges, such as the New York Stock Exchange.

BaFin supervises credit institutions – together with the Deutsche Bundesbank and, in some cases, the European Central Bank – financial services institutions, insurance undertakings, pension funds and asset management companies. Supervising stock exchanges, on the other hand, is entrusted to the stock exchange supervisory authorities of the Federal States.

BaFin and the SEC both supervise security issuers and transactions on the financial markets (market supervision), including the monitoring of the ban on insider trading and compliance with transparency requirements. However, the SEC’s market supervision is more comprehensive, since its tasks also include charging violations which would constitute capital investment fraud pursuant to section 264a of the Criminal Code (Strafgesetzbuch) under German law. In Germany, only criminal prosecution authorities are competent for such charges. In addition, both BaFin and the SEC are competent to register/approve securities prospectuses.

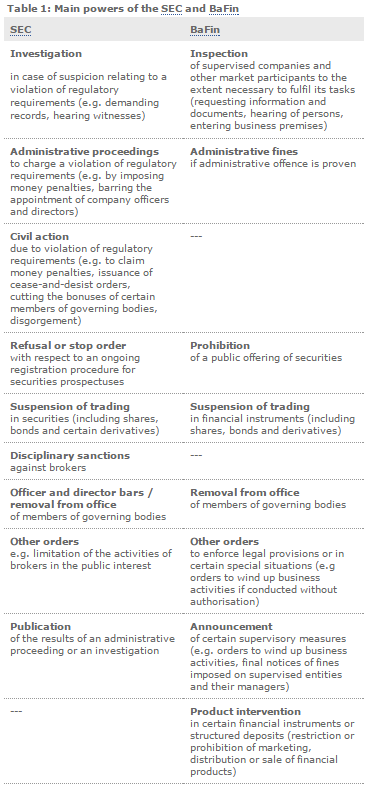

Important powers

Both authorities have extensive powers. The SEC’s powers are stipulated in the US Securities Act and Securities Exchange Act, those of BaFin in various financial market laws, such as the Securities Trading Act (Wertpapierhandelsgesetz – WpHG), the Banking Act (Kreditwesengesetz – KWG), the Insurance Supervision Act (Versicherungsaufsichtsgesetz –VAG) and the Securities Prospectus Act (Wertpapierprospektgesetz –WpPG).

The powers of the SEC and BaFin are generally comparable. However, one key difference is the ability of the SEC to file civil actions. BaFin does not have such an ability. This, in part, results from the fact that German administrative authorities may enforce their orders by themselves, using compulsory administrative enforcement and, thus, are not dependent on obtaining a court order to fulfil their tasks.

The far-reaching investigatory powers of the SEC are also significant: by issuing a subpoena, it may request the production of documents and summon persons to a hearing. US courts impose severe sanctions in case of non-compliance with a subpoena, which may include imprisonment of the non-compliant person. By contrast, although BaFin has no comparable “subpoena power”, it may enforce its orders through coercive measures, for example by taking the necessary measures itself or via direct enforcement, such as with the help of enforcement officers. However, in an investigation of potential violations, a coercive fine is regularly considered. Such a fine may amount to up to EUR 250,000, with higher amounts possible in certain cases. If the coercive fine is not paid, BaFin may apply to the competent court to order imprisonment under certain conditions. If a person fails to comply with an enforceable order of BaFin to produce documents or to appear at a hearing, BaFin may, in addition, impose an administrative fine (section 39 (3) no. 1 (a) and (4) in conjunction with section 4 (3) sentence 1 of the WpHG). If a criminal proceeding is initiated under capital market law, moreover, the investigative powers of the criminal prosecution authorities, which are also far-reaching, come into play in Germany.

The powers of the SEC and BaFin to suspend trading in securities and regarding the registration/approval of securities prospectuses as well as with respect to the removal of members of governing bodies from office are largely comparable. Unlike the SEC, BaFin’s remit also allows it to remove members of governing bodies of credit institutions and insurance undertakings.

Incidentally, there are qualitative differences between the powers. For example, unlike BaFin, the SEC may obtain disgorgement by way of civil action and cut the bonuses of certain members of governing bodies.

Money penalty amounts in the US

The measurement methods and the size of the money penalties imposed by BaFin and by the SEC, or by the US civil courts, are different as well.

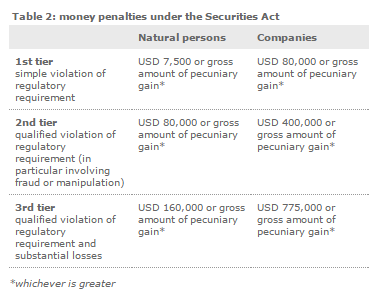

The Securities Act provides for a three-tier sanction regime for money penalties which may be imposed by the SEC following the conclusion of an administrative proceeding and by the federal courts following a successful civil action brought by the SEC. The size of the penalty depends on the severity of the violation and the size of the loss as well as whether the subject of the penalty is a natural person or a company.

According to its own press release, in the fiscal year 2014 the SEC filed a total of 755 enforcement actions to sanction violations of capital market provisions. It obtained orders totalling USD 4.16 billion in disgorgement and penalties. However, this sum includes the settlements agreed by the SEC, because of which a comparison of the track record of the SEC and BaFin cannot be based solely on the total amount of penalties imposed. There are few limits to the size of settlement amounts under US law. The SEC particularly focuses on efficiency considerations when agreeing to settle enforcement actions. Thus, it may end investigative proceedings without needing to initiate and carry out an administrative proceeding or a civil action, thus gaining capacity for the investigation of other violations.

In recent years, US civil courts have repeatedly criticised that SEC settlements generally do not require an admission of wrongdoing and that settlement amounts were too small. The SEC has changed some of its practice in response. It now accepts settlement agreements for serious violations only if these contain an admission of wrongdoing. However, critics continue to call for higher settlement amounts.

For its part, BaFin does not have the ability to conclude comprehensive settlements. So-called “agreements” (Verständigungen) may be concluded in administrative fine proceedings. These are a sort of amicable settlement in an administrative fine proceeding, particularly for reasons of procedural economy. According to its supervisory practice, BaFin may grant a reduction in the fine of up to 30% depending on the stage of the proceedings. It is not possible to conclude agreements that end the administrative fine proceedings without a verdict.

Administrative fine amounts under German law

Under German law, the size of the fine depends on what degree of penalty the law envisages for the specific offence leading to the fine. Certain administrative offences pursuant to the WpHG currently provide for fines of up to EUR 1 million per violation. Pursuant to the KWG, in certain cases fines of up to EUR 5 million per violation may be imposed. BaFin recently made use of its ability to impose comparatively large fines. If the fine is not large enough to offset the economic benefit gained from the violation, it may be increased to 10% of net sales in the fiscal year prior to the violation for companies, or to double the pecuniary gain from the violation, whichever is greater. The size of the administrative fines for some matters covered by the WpHG will also be increased to a similar level as a result of the implementation of the new EU financial market regulation.

In 2014, BaFin imposed fines totalling almost EUR 4 million in 178 proceedings for violations of securities laws (see BaFin Annual Report 2014). These figures cannot be directly compared with those of the SEC. The moderate size of the fines is explained by the fact that under German law, serious violations of capital market laws are generally sanctioned under criminal law. BaFin brings violations of the prohibitions of market manipulation and insider trading, in particular, to the attention of the relevant public prosecutor’s office if sufficient initial suspicion is present. In the US, the Department of Justice is responsible for the prosecution of capital market crimes, but it is normal for matters to be investigated simultaneously by the Justice Department and the SEC, possibly with differing sanctions as a result.1

Other legal sanctions

In addition, in Germany and other EU Member States there are other sanctions for violations of law which can have an even stronger effect than fines. US capital market law is not familiar with the so-called forfeiture of shareholder rights, for example: significant shareholders who hold shares in an issuer from Germany cannot exercise the voting rights from their shares as long as they have not complied with the notification requirements pursuant to the WpHG (forfeiture of voting rights). The forfeiture of voting rights may lead to shareholders’ resolutions of affected issuers being challenged and possibly being declared void, if obtained on the basis of votes invalid due to a forfeiture of rights. Moreover, the right to dividends is suspended if the reporting requirements are deliberately breached. Only if failure to notify was not deliberate and the notification is subsequently submitted does the shareholder retain his right for dividends. The forfeiture of rights is an additional motivation for market participants to comply with their reporting requirements.

BaFin’s additional powers

Apart from the repressive sanctions which are imposed after a violation, BaFin’s inspections and supervisory interviews have an important preventative effect on the companies supervised by it. They help to identify violations of legal provisions at an early stage and to remedy them. An important tool available to BaFin to ensure compliance with the law is especially the ability to express disapproval to, or to caution members of, the governing bodies of supervised companies.

Since the German Retail Investor Protection Act (Kleinanlegerschutzgesetz) came into force, BaFin has also got the ability pursuant to section 4b of the WpHG to restrict or prohibit the marketing, distribution or sale of certain financial instruments or structured deposits. It may consider doing this if the financial instrument or structured deposit gives rise to significant investor protection concerns, poses a threat to the orderly functioning and integrity of financial markets or commodity markets or to the stability of the financial system. There is no such product intervention power in US capital market legislation. This development will contribute to strengthening the public perception of BaFin as what it is: a supervisory authority with effective powers.

Footnote:

1) Although the SEC and the Justice Department sometimes work together on investigations, they are independent authorities whose powers overlap in some areas. Unlike in German law, US legislation is less concerned with precisely reconciling the areas of competence of the capital market supervisor and the criminal prosecution authorities.

Source: BaFin – BaFin and the SEC: An international comparison of supervisory practice

Related Posts

CFTC signed MOU with BaFin and Bundesbank to enhance supervision of cross-border clearing organizations

CFTC signed MOU with BaFin and Bundesbank to enhance supervision of cross-border clearing organizations New President of the German Financial Supervisory Authority (BaFin)

New President of the German Financial Supervisory Authority (BaFin) German supervisory authority warns for the Forex provider XMarkets

German supervisory authority warns for the Forex provider XMarkets Regulators from around the world issued warnings for unauthorised financial services companies

Regulators from around the world issued warnings for unauthorised financial services companies- Financial Regulators around the world warn for unauthorized financial services firms