Royal Bank of Scotland announces Updates to the Market and Banco Santander publishes 2015 Results

The Royal Bank of Scotland Group plc (“RBS” or “the Group”) today announces a series of updates to the market:

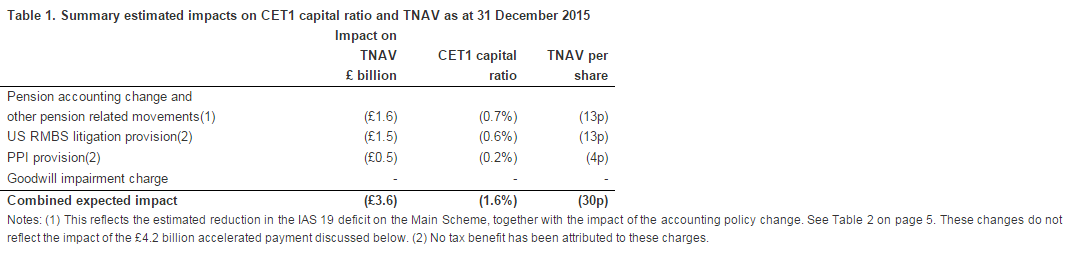

1. Developments during 2015, in particular publication by the International Accounting Standards Board of its exposure draft of amendments to IFRIC 14 IAS 19 – The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction, have provided additional clarity on the role of trustees’ rights in an assessment of the recoverability of a surplus in an employee pension fund. In the light of this, RBS has revised its pension accounting policy for determining whether or not it has an unconditional right to a refund of any surpluses in its employee pension funds. This change will result in the accelerated recognition of £4.2 billion of already committed future contributions in respect of past service. This is expected to result in an accounting deficit of £3.3 billion as at 31 December 2015 relating to the main section of The Royal Bank of Scotland Group Pension Fund (the “Main Scheme”). The net, post tax impact of this policy change, together with updated IAS 19 valuations, on Tangible Net Asset Value (“TNAV”) is approximately £1.6 billion, largely recognised in the Statement of Other Comprehensive Income by way of a prior year adjustment. These changes will reduce TNAV per share at 31 December 2015 by a net 13p and reduce the Common Equity Tier 1 (“CET1”) capital ratio by approximately 0.7%.

Separately, RBS has signed a Memorandum of Understanding with the Main Scheme Trustee (the “Trustee”) to make a payment of £4.2 billion into the Main Scheme, being an accelerated payment of existing committed future contributions. The majority of this payment has been provided for as a result of the accounting policy change described above. The incremental impact of making this one-off payment in 2016 is expected to be a further reduction of around 3p on TNAV per share and a further CET1 capital ratio reduction of approximately 0.3%. The accelerated payment is expected to both improve RBS’s capital planning and resilience through the period to 2019 and provide the Main Scheme Trustee with more flexibility over investment strategy.

2. An additional provision of $2.2 billion (£1.5 billion) in relation to various US residential mortgage-backed securities (“RMBS”) litigation claims in Q4 2015 which will reduce attributable profits for Q4 2015 by £1.5 billion, reduce TNAV per share at 31 December 2015 by 13p, and the CET 1 capital ratio by 0.6%.

3. An additional provision of £500 million in relation to Payment Protection Insurance (“PPI”) in the context of the recent FCA consultation paper CP15/39, which will reduce attributable profits for Q4 2015 by £500 million, reduce TNAV per share at 31 December 2015 by 4p, and the CET 1 capital ratio by 0.2%.

4. A Q4 2015 goodwill impairment charge of £498 million in respect of its Private Banking business. This will reduce attributable profits in Q4 2015 by £498 million, but as an intangible item will have no impact on TNAV per share or the CET1 ratio.

As at 31 December 2015, RBS expects to report a CET1 capital ratio of approximately 15% and TNAV per share of approximately 350p versus a CET1 capital ratio of 16.2% (pro-forma for the full disposal of Citizens) and TNAV per share of 384p as at 30 September 2015, pending the completion of normal year end processes. These figures are preliminary estimates and unaudited.

Subject to PRA approval, we expect the adverse core capital impact resulting from the proposed pension accounting change, including the £4.2 billion accelerated payment, to be partially offset by a reduction in RBS’s core capital requirements. The timing of any such potential core capital offsets are likely to occur at the earliest 1 January 2017, and will depend upon PRA’s assessment of RBS’s core capital position at that time.

RBS CEO Ross McEwan said:

“I am determined to put the issues of the past behind us and make sure RBS is a stronger, safer bank. We will now continue to move further and faster in 2016 to clean-up the bank and improve our core businesses. We’ve always been open about the scale of past issues facing RBS and although there is clearly much more to do, this announcement is a further step towards addressing legacy issues and building a great bank for our customers and delivering long term value for our shareholders.”

Banco Santander has issued an announcement to inform in relation to 2015 Results. According to the bank statement:

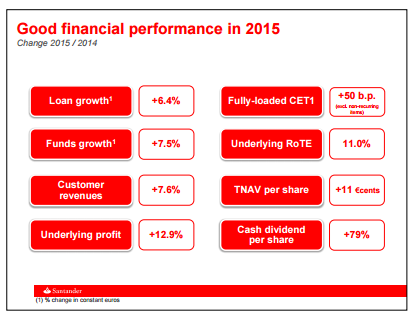

Banco Santander delivers on its targets andm earns EUR 5.966 million (+3%), with strong munderlying performance of 13% based on mincreasing customer satisfaction and loyalty

- “In 2015, we have delivered ahead of plan in the right way, growing revenues by improvingcustomerservice and increasing loyal and digital customers.

- Growth in underlying revenues and profits has resulted in a ROTE of 11%, which has allowed us to pay 79% more cash dividend per share, increase the net asset value of our shares by 3% and strengthen our capital position organically – thereby delivering on commitments we made when we raised capital last year.

- We continued to help our clients, both individuals and businesses, prosper through access to credit, which grew 6%. During 2015 we also executed on our commercial transformation to become more simple, personal and fair.

- Loyal customers grew by 1.2 million, to 13.8 million, and digitally active customers by 2.5 million, to 16.6 million.

- We are confident that we will reach the targets we set for 2016.” Ana Botín, Group executive chairman, Banco Santander

- CUSTOMERS. Credit volume grew 6%, to EUR 805,395 million, boosted mainly by Latin America and SCF. Deposits and mutual funds, which totalled EUR 774,819 million, were up 7% compared to 2014.

- RESULTS. Commercial revenues grew more than costs, around 8%, while loan-loss provisions fell 4%. Our P&L reflects prudence in management, as non-recurring earnings of EUR 1,118 million were assigned to non-recurring items (EUR 1,718

- million).

- CAPITAL. Regulatory CET1 stood at 12.55%, significantly exceeding the minimum required for 2016 (9.75%). The fully loaded CET1 increased 40bps in the year, to 10.05%, on target to exceed 11% in 2018.

- DIVERSIFICATION. Europe contributed 56% to Group profit (UK, 23% and Spain, 12%) and the Americas, 44% (Brazil, 19% and U.S., 8%).

– Spain: attributable profit amounted to EUR 977 million (+18%). Lending to companies and SMEsincreased 1% while customer funds grew 1% for the year.

– UK: attributable profit stood at EUR 1,971 million (1,430 million pounds, this is before PPI, up 14%). Lending grew 5% and customer funds, 6%.

– Brazil: attributable profit totalled EUR 1,631 million (5,946 million reais, up 33%). Lending grew 9% and customer funds, 12%.

Banco Santander registered attributable profit in 2015 of EUR5,966 million, a 3% increase compared to 2014. Underlying profit, which does not include the effect of non-recurring results, grew an additional ten points, by 13%, and reached EUR 6,566 million.

In a year marked by a complex international economic scenario, with record low interest rates in currencies key to the Group such as the euro, pound and dollar, Banco Santander maintained positive performance. Lending increased 6% and customer funds rose 7% resulting in commercial revenues growing 8% and underlying profit, 13%.

Growth in business and results allow the bank to distribute a dividend per share of EUR 0.20, of which EUR 0.16 is in cash, 79% more than 2014. Dividend yield at current share prices is around 5%. Furthermore, the bank fulfills its commitment to increase tangible net asset value per share (TNAV), which increased by 3% since the close of 2014, to EUR 4.12.

These figures mean the bank is on track to achieve the targets announced by Santander’s management team at the September 2015 Investor Day. Key goals were set to reach a core capital ratio above 11% and ordinary RoTE of 13% by the end of 2018. Today, core capital is above 10% and ordinary RoTE is 11%.

Improved performance in revenue and business was backed by progress achieved in the Group’s commercial transformation supported by technological improvements and digitalization. Thus, the number of loyal customers grew 10%, to 13.8 million, with notable increases in Mexico (+14%) and the UK (+11%).

Digital customers increased 17%, to 16.6 million, so that 31% of the Group’s total customers can be considered digitally active. Mobile users that use the bank´s app an average of 13 times per month increased 50%, to 6.9 million. The volume of digital transactions rose 58%.