Coronavirus and credit – a perfect storm

This article posits that the spread of the coronavirus coincides with the downturn in the global credit cycle, with potentially catastrophic results. At the time of writing, analysts are still trying to get to grips with the virus’s economic impact and they commonly express the hope that after a month or two everything will return to normal. This seems too optimistic.

The credit crisis was already likely to be severe, given the combination of the end of a prolonged expansionary phase of the credit cycle and trade protectionism. These were the conditions that led to the Wall Street crash of 1929-32. Given similar credit cycle and trade dynamics today, the question to be resolved is how an overvaluation of bonds and equities coupled with escalating monetary inflation will play out.

This article sees worrying parallels with the collapse of John Law’s Mississippi scheme exactly 300 years ago. By tying in the purchasing power of his livres to the value of his Mississippi venture, Law ensured they both collapsed together in the space of only six months.

The similarities with our Keynesian experiment are too great to ignore. Could a simultaneous collapse of fiat currencies and financial assets happen again? If so both the money bubble and financial asset bubble could be fully deflated into worthlessness by this year’s end.

The epidemic

“Ring-a-ring o’ roses / A pocket full of posies / A-tishoo! A-tishoo! / We all fall down.”

Some folk attribute this old nursery rhyme to the plague in England of 1665. But it seems singularly appropriate for coronavirus or COVID-19, about which, as yet, we know little. Its origin is, allegedly, a mutation of a virus from a snake, bat or pangolin. Alternatively, one school of thought believes it escaped from a biological warfare laboratory in Hunan. At the time of writing, officially, the ratio of reported deaths to reported recovered is about 23%, which has been declining as time progresses.[i] While the fatality rate is expected by Western analysts to level out at about 3.5-4% of those infected, its spread is probably much more serious than admitted, with the Chinese being accused of playing the crisis down. To be fair, it will have been hard for the authorities to keep up with its rapid spread. Coming during the Chinese New Year holiday when most factories have closed anyway, there is some confusion about the economic impact. Officially, the public holiday ended on 30 January, but nearly all factories were still closed a week later, and their reopening will be gradual at best.

Not only do Chinese factories supply the world with consumer goods, but they are integral to global supply chains. Hyundai in South Korea has already been forced to close all its factories due to lack of Chinese components and other car makers around the world have expressed similar difficulties. For all intents and purposes, China is shut, and therefore its economy is not functioning. And the longer this goes on it is increasingly difficult to see when, if ever, past normality will return.

China’s experience threatens to be repeated elsewhere, in which case the world, with closed factories and people severely restricted in their human interactions, faces the deepest global economic slump since medieval times, when the plague ravished Europe. Ring-a-ring o’ roses indeed. Meanwhile, financial assets stand close to all-time highs. This is undoubtedly due to money and credit being pumped into financial markets at a quickening pace, and while bond yields are suppressed by freely available money, it seems economic actors prefer not to hold bank deposits relative to the risk of holding equities.

Just when this viral epidemic materialised, the financial system was already on life support and at its weakest. The credit cycle is due to turn down, and the dynamics behind it suggest it could be worse than the Lehman crisis, which was broadly contained to financial entities and residential property prices. This time the banks have accumulated worrying levels of junk debt directly and indirectly through collateralised loan obligations. Money markets are badly stretched with liquidity having miraculously disappeared. Central banks are flooding them with new money even before the periodic banking and systemic crisis has occurred. But all this extra central bank money achieves is to drive financial asset values even higher.

It will be a mistake to blame the financial and economic events that follow on the coronavirus, but inevitably this is what those who have relied on a failing monetary system will do. As to the course of the coronavirus epidemic, only time will tell. With financial markets already teetering on the edge of a systemic and economic crisis, the timing of its emergence could pull the trigger on a global financial and economic collapse.

The credit cycle and asset inflation

We should remind ourselves that the credit cycle, which is the manifestation of banking psychology in changes in the availability of credit, is on the turn. There are three distinct classifications of credit demand affected: the non-financial economy, speculators (particularly large hedge funds) and governments.

Commentary by financial pundits almost exclusively concerns the non-financial economy, with monetary policy officially targeting consumer prices and employment. The encouragement of banks to lend is part of it. By creating an artificial boom, banks are further persuaded to increase their lending at suppressed rates, leading to a misallocation of capital resources. Prices of consumer goods then begin to rise, and interest rates with them, undermining the basis of business calculation. Sensing increased loan risk, the banks begin to restrict the expansion of bank credit, which only increases credit risk even more. Banks begin to panic, withdraw revolving credit facilities and consequently they drive the economy into a slump.

That is a brief summary of the classic credit cycle, but it bears little relation to that of today. Instead of bank credit being predominantly deployed for production, it is increasingly taken up by financial intermediaries lending to consumers. Furthermore, consumers have reduced their deferred consumption in the form of savings, which in former times were integral to the workings of the credit cycle. And despite central bank propaganda about being primarily interested in the non-financial economy, this sector has become progressively demoted relative to the funding needs for financial speculation in order to maintain asset values and sustain government borrowing.

Today, in the US, UK and many other developed economies, with the exception of pension and insurance funds, savings as an economic force have virtually disappeared. The majority of consumers are now living pay-day to pay-day and continually in debt with respect to their current spending. Predominantly at the expense of ordinary people, wealth and real income have been increasingly transferred from productive individuals to governments, the banks and their favoured borrowers through monetary debasement. The effects of monetary debasement have been concealed by statistical method, leaving consumers considerably worse off than slavish followers of government statistics are generally aware.

Every credit cycle impoverishes consumers even more, as their earnings and diminishing savings are continually eroded by ever accelerating monetary debasement. Having tamed the statistics, governments such as the US, the UK and some members of the EU now think they can abandon all fiscal probity. They think they can finance budget deficits, public investment projects and even sustainable energy projects with only limited consequences for the currency’s purchasing power, all by inflationary means. It is, of course, all delusion, consistent with end of cycle psychology.

The reality is government spending is out of control. The net present values of future welfare commitments are materialising in the form of current liabilities. Governments are funded by the expansion of their central banks’ balance sheets. The only thing keeping this illusion going is the activities of speculating hedge funds leading directly and indirectly to continually rising financial asset values.

But there is a crunch coming. It appears to have started to arrive last September, when the US repo market suddenly seized when the overnight rate spiked up to ten per cent. Such are the accelerating demands of government funding that they cannot be accommodated as well as the interest arbitrage activities of the speculators active in repos and foreign exchange (fx) swaps.

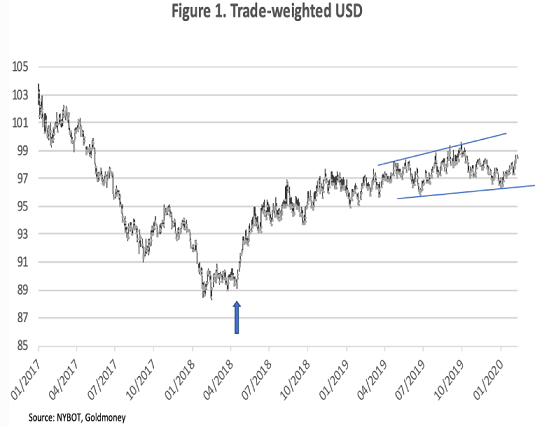

The speculators, particularly the big relative value hedge funds, turned bullish on the dollar in April 2018, three months after President Trump took office. It was clear, to the speculators at least, that his proposed tax cuts would stimulate the economy, drive up government borrowing rates, and therefore foreign demand for dollars to invest in US debt at a time when euro and yen interest rates were trapped under the zero bound. That point is marked by the up-arrow in Figure 1 below, when a clear breakout in the dollar’s Trade-Weighted Index took place.

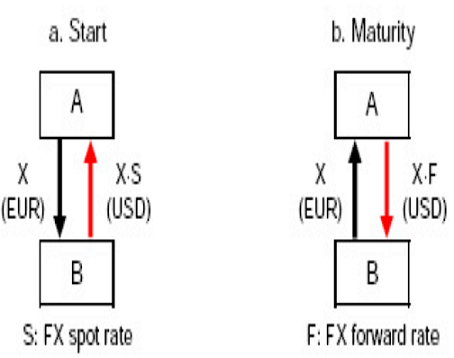

The dollar’s trade-weighted index is heavily weighted in favour of the euro. Since the ECB had pegged its interest rates below the zero bound, it gave rise to an immensely profitable trade. A speculator could borrow euros at close to zero interest rates to buy US Treasury bills and even coupon-paying bonds for a yield pick up of over 1.5% in April 2018, rising to 2.39% for T-Bills a year later as the Fed tried to reduce its balance sheet. Much of this trade is conducted through fx swaps, which lock in interest rate differentials for as long as a year (sometimes more) and whose 10% deposit for the forward leg allows a speculator to gear the trade up ten times. The basic mechanism is shown in the schematic illustration below (courtesy of The Bank for International Settlements).

Putting counterparty risk aside, this is seen by hedge funds as a riskless trade, with the leg at maturity fixed at the outset. Therefore, it operates much like a repo. But it should be noted that when the trade is unwound, changes in the value of the collateral and the exchange rate have to be absorbed directly or indirectly by the swap provider.

Rising bond yields and a fall in the dollar exchange rate will have significant consequences for swap availability. Meanwhile, according to The Bank for International Settlements, FX forwards and swaps outstanding grew from $53.9 trillion to $59.4 trillion in the first half of 2019, the vast majority involving dollars. Given the increasing popularity of this trade it is likely to have grown further into the year-end. It is now straining the resources of the banking system to lend dollars as part of swap arrangements at the same time as the primary dealer subsidiaries of the G-SIBs have to hold increasing quantities of inventory of US Treasury bills and bonds.

We must also consider the currency effect. Because the trade requires the FX swap counterparty directly or indirectly to short euros or yen for dollars and to invest them in T-bills and short maturity US Treasuries, the effect has been to depress the euro and the yen while increasing demand for dollars. So much so, that the trade imbalances that favour the euro and yen and strongly disfavour the dollar have not been uppermost in currency pricing. Normal trade related supply and demand has been swamped by speculative demand for the dollar.

But as the chart in Figure 1 suggests, the dollar’s bullish momentum is now stalling. The strains on the banks, particularly the global systemically important banks (G-SIBs) who under Basel III rules have to demonstrate sufficient liquidity to cover all forward liabilities thirty days in advance, are now capacity constrained. The signal for this liquidity crisis occurred on the same day as Deutsche Bank sold its prime brokerage to BNP, suggesting there may be other risk elements in the mix. For the dollar, the consequence is that unless demand for fx swaps continues to be supplied, it will begin to decline.

The Fed had no alternative but to step in and through repos provide extra liquidity to the G-SIBs, which it has been doing since September at a wildly fluctuating daily amount, recently averaging about $50bn. To the extent the G-SIBs are now reliant on the Fed’s repos, they act as a pass-through to the speculating hedge funds. In effect, the Fed is directly supporting the speculating hedge funds in their activities and is now the primary agent behind the inflation of financial asset prices.

Whether it is by default or intent, the Fed has effectively welded the dollar’s purchasing power to the values of financial assets. They are both rising together and will almost certainly fall together. The only question is which will take the lead.

The Fed’s policy of inflating financial assets has taken them into severely overvalued territory. The reality being ignored is that governments, particularly the US Government which with its reserve currency sets the valuation basis for all markets, have only short-term solvency available by debauching their currencies. Raising taxes instead would be ruinous for the underlying economy, and cutting spending goes against the expressed wishes of central banks looking for fiscal stimulus.

The rating of the US Government’s debt is wholly incompatible with the facts. Worse, when markets begin to reflect on this contradiction, they will realise that the higher the cost of funding goes, the higher it will then go. The US Government is firmly ensnared in an inescapable debt trap. And as time passes, the only alternative to government spending grinding to a halt will be to continually accelerate currency debasement.

Meanwhile, the tranquillity of financial markets everywhere belies their biggest challenge yet. The impact of the coronavirus on China’s economy, and therefore the global economy should not be lightly dismissed. Even if it does not become a pandemic, defined as an epidemic across national borders, it comes at a time when the global economy is entering the crisis stage of the latest credit cycle. The fact that these two events have also coincided with a collapse of cross-border trade, brought about by President Trump’s tariffs against China, gives an added viciousness to the situation. Even without the virus, the similarities with 1929 leading to the Wall Street crash and the subsequent economic depression, should give thinking investors considerable pause for thought.

The great awakening

If our thesis is correct, that being bound together the purchasing power of the dollar and values of financial assets will probably collapse at the same time, we will see a different outcome from that which might otherwise be expected. Today, anyone discussing the consequences of monetary inflation would suggest the currency’s purchasing power will decline over a period of several years at an accelerating rate, giving those who recognise what’s happening time to protect themselves. This was the experience in Germany and some other European nations in the wake of the first World War. Instead, if it happens as described herein, the collapse will be extremely rapid, with bonds, equities and unbacked state currencies collapsing together in the space of less than a year. All that’s required is for the private sector to stop buying government bonds.

It has happened once before, exactly three hundred years ago. Like the central banks of today dealing with their governments’ debt, John Law in Paris had used the inflation of his own banknotes to ramp up the price of the Mississippi Company shares. By December 1719 Law’s scheme had begun to hit headwinds: the flood of his printed money into Mississippi shares fuelled profit taking. Law’s unbacked livres entered general circulation and led to a rise in price inflation.

The factor that finally undermined his scheme was the young King selling out the royal holding of 100,000 shares at 9,000 livres on 28 February for staged payments. It was a combination of a signal and too much supply for the market to bear, and both the shares and Law’s paper livres began to collapse. By the following September, while Mississippi shares still had a notional value of a few thousand livres, the livres were worthless.

The collapse of the currency preceded that of the shares by just a few months. Today, a similar tiredness around currencies prevails, whose purchasing power governments wittingly or unwittingly conceal. In recent years, price inflation in the United States has been running at about 10% in most major cities, based on evidence from independent analysts, not the goal-sought 2% of official figures.[ii] Given the standardisation of CPI method, we can assume price inflation in other jurisdictions is similarly understated. But we have yet to see the purchasing powers of unbacked fiat currencies begin to accelerate in their decline, as appeared to be the case in late-1719.

No matter. Instead, we should assess likely changes in monetary policy in the coming months. This time, we have the additional damage done to human interaction by the coronavirus. China’s economy, where production is ceasing and food prices are rocketing, could be evolving into a John Law-like collapse, in which case the currency will be next. Commentators are saying that once the virus passes, everything will return to normal. It won’t because the lies and hype that go with paper money will almost certainly have been exposed, as John Law found to his cost.

We can see that, rather like King Louis cashing out of John Law’s scheme in February 1720, in China the bullish spell is being challenged by the coronavirus. And China matters, being the world’s largest producer of consumer and intermediate production goods in the world. The Chinese government are expanding the money quantity rapidly to support the stock market and will also do so through state-owned banks in a vain attempt to support the wider economy. Just like John Law in those final three months.

The signal that it’s all going wrong for the yuan is likely to be reflected in demand for bitcoin, which can be bought online through peer-to-peer marketplaces, even by punters under quarantine (Chinese bitcoin exchanges were shut down by the government in 2017). At the time of writing, they were trading at a small premium to the dollar price. If that premium increases, or the number of bids suddenly jumps, it will be an indication that Chinese residents are beginning to lose faith in their currency. If the authorities try to ban peer-to-peer bitcoin sites, it will send a similar signal.[[iii]Even without the coronavirus spreading to other nations and undermining their economies directly, those who believe in the efficacy of their central bank’s monetary policy will begin to have doubts as not even negative interest rates have succeeded in stopping an economic decline. The error came from unswerving beliefs in the inflationary policies of John Law and John Maynard Keynes.

The effect on the dollar

Doubtless, there will be those in the American administration who will see in China’s economic woes an opportunity to re-establish American production. But they will be blind to a far greater consequence: a global slump in consumer demand. It was already in the making; the credit cycle having turned and global trade demonstrably shrinking.

The greater danger for the Americans is a realisation that with a global economic slump that cannot be denied, overvalued stock prices are vulnerable to a major fall. At the same time, there is likely to be a sharp reassessment of the government’s borrowing requirements. At that point, the link between overvalued stocks and unrealistically low government bond yields can only lead to one conclusion: reliance on unlimited quantitative easing as the means of funding government spending will appear endless.

Earlier in this article it was noted that hedge funds were playing the fx swap game to the extent that the G-SIBs’ balance sheets had become overstretched, and that the Fed was now providing the necessary liquidity for these positions to be maintained. It would be dangerous for these speculators to assume the Fed will continue through the G-SIBs to fund their fx swaps. The G-SIBs themselves are increasingly likely to withdraw from providing unlimited fx swap facilities as the whole game stalls.

Assuming this is the case, on a net basis fx swap positions will have to be unwound, leading to an additional supply of T-bills and short dated Treasuries, dollar selling and the closing of euro and yen short postions. A weakening dollar and falling Treasury bond prices can only be avoided if foreign buyers step up to buy them. But with the collapse in global trade that was already evident before the coronavirus, they have no need to do so. They have levels of dollar liquidity and ownership that are more than enough for their needs and so they are likely to be sellers at the same time as fx swaps are being unwound. US-centric analysts and commentators are unprepared for this event.

The myth they believe in is the Triffin dilemma’s protection for the dollar, whereby foreigners will still be forced to continue to buy it because it is the reserve currency. Conveniently the believers in Triffin’s dilemma fail to acknowledge Robert Triffin’s conclusion: that foreign claims on the dollar would accumulate to the point where a run on it would inevitably occur. Triffin feared that the inevitable rise in US dollar interest rates that follow would cause global deflation.

If Triffin was right, it fits in with our analysis. The only amendment to his theory we can permit is his conclusion of deflation, but then he wrote at a time when a gold standard existed. If by deflation he presumed a slump in economic activity, we are bound to agree. If, as the term implies, he means a contraction in money quantities, we must disagree. For surely, faced with a US Government desperate for funds, and if it is not already in a state of collapse a banking system with liquidity problems, the Fed’s monetary response will be to provide however much it takes out of thin air.

It’s not just Triffin. John Law was the forerunner of Keynes, who similarly understood that an economy could be stimulated by monetary and credit expansion but failed to find a solution to the eventual fallout. In Law’s case, his expansionism was not repeated until the time of the French revolution, a very different situation. In Keynes case, we have seen the build-up of destabilising credit cycles over a longer period, but the result seems bound to be the same.

[i] See https://gisanddata.maps.arcgis.com/apps/opsdashboard/index.html#/bda7594740fd40299423467b48e9ecf6

[ii] See Chapwood Index at chapwoodindex.com, and Shadowstats at shadowstats.com

[iii] Local bitcoin prices in China can be checked here: https://localbitcoins.com/places/7091996/shanghai-china/

By Alasdair Macleod, www.goldmoney.com

Find more: Contributing Authors