EUR and GBP Are Committed To CFTC Reports

The world has been spoiled by the beautiful game for the past four weeks, and yesterday’s final, although not a classic, the most consistent team was crowned champion. Football was the winner along with sportsmanship. Can the markets now get down to some business? All the various asset classes have suffered during the tourney, all robbed of sustainable ‘volume and volatility’ over the past few weeks and worse, the beginning of the summer doldrums has not even truly begun yet. It’s a big ask for the first day with so many apparently recovering from a World Cup hangover.

Central Banks Dominate

This week is dominated by a plethora of Central Bank activity, enough to grab all investor’s attention. Later today, ECB’s Draghi speaks to the European parliament and many expect him to release more details about the TLTRO’s. The RBA minutes are released tomorrow, and should keep investors on their toes especially with Governor Stevens jawboning his currency down of late. Ms. Yellen from the Fed is front and center both Tuesday and Wednesday, where she is expected to maintain her ‘dovish’ tone, while looking through the inflation noise. The BoC, hot on the back of a dismal Canadian employment report last Friday, are expected to keep rates on hold and remain ‘dovish’ despite stronger CPI data of late.

On the handover from Europe, sellers are leading the latest price action, although pressure and interest is again limited due to “Bastille Day” in France, Europe’s second largest economy. The UK Gilt bond bear will be looking to events later in the week where the UK June unemployment data on Wednesday is forecasted to see the unemployment rate for the three months up until May fall further to +6.5%. On Tuesday, UK inflation data for June is expected to tick a tad higher (+1.6% vs. +1.5%) from its four and a half-year low print the previous month. Governor Carney and a few fellow cohorts will also get to answer question from the UK Treasury select committee about the Financial Stability Report on Tuesday. Until all is revealed, investors and dealers will be relying on the range trade from a fix-income perspective.

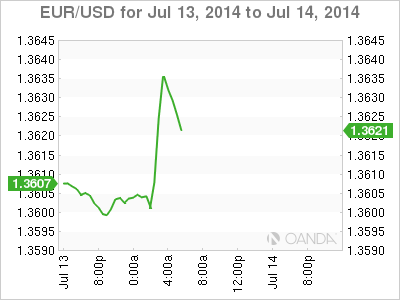

Is the EUR the Funding Currency of choice?

The pound (£1.7117), from a broken record perspective, is likely to remain well supported in the short-term, as the UK economic outlook remains positive (in comparison) and the BoE is edging closer to hiking interest – well before their compatriots. Despite the UK’s large current account deficit remaining a concern, the country’s economic growth remains strong and coupled with the perception of higher rates (to attract further foreign investment); it will be able to support GBP going forth against most low yield back currencies. The EUR (€1.3621) is expected to remain under pressure for the ECB’s monetary policy. Yield differentials should continue to put further downward pressure on EUR’s money market rates and encourage must stronger use of the EUR as a funding currency – follow the EUR cross for direction.

EURO Spreads tighten

The 18-member single currency has held its one so far this morning. The EUR (€1.3636) has managed to nudge up to a fresh intraday high versus its G10 peers. Aiding the currency are the main Euro bourses trading in the ‘black,’ while the euro-zone peripheral spreads tighten a tad (Portugal/Bund is outperforming, especially with the shares from Portugal’s BES opening higher). Both 10-year Spain/Germany and Italy/Spain have both managed to come in a bit after last weeks potential blowout scare. Even this morning’s Euro-zones industrial production has beaten expectations – down only -1.1% for May vs. -1.2%. National manufacturing weakness already recognized and had been mostly priced in. The EUR bear continues to be caught in this tight trap with many looking for further guidance form the ECB for some positional vindication. Currently, the EUR’s topside looks the most vulnerable, with the July 10 high (€1.3651) the markets next point of reference. On the downside, the single unit has to contend with the 80′s, the €1.3585 with some momentum to justify these shorts outright. Following the major EUR crosses, it’s less tedious and certainly more informative. Watch Gold and the EUR/JPY squeeze, any of these positional changes gives the investor a better insight, especially when the EUR follows.

CFTC commitment of traders

The latest report reveals that the net USD positions have been trimmed again, by -$0.4b to +$2.1b. This was probably done on the back of the latest NFP report where payrolls increased by +288k vs. +215k forecasted. Other notable currency positions shifts: Kiwi (NZD) the net longs increased after the July 8th Fitch upgrade. This will certainly be a squeeze; the report noted a big uptick in CAD, turning longs for the first time since Feb 2013. What poor timing, especially after last Friday’s horrid jobs report that saw the loonie fall from grace very quickly and remain trading well north of the psychological $1.0700 level. The EUR saw net short rising slightly, while net GBP longs were trimmed on some profit booking (still the largest interest).

Source: marketpulse

Related Posts

Morgan Stanley: Central Banks Are Playing a Game of Chess That Results in an Endless Cycle of Easing

Morgan Stanley: Central Banks Are Playing a Game of Chess That Results in an Endless Cycle of Easing Draghi and Yellen leave EUR/USD in range

Draghi and Yellen leave EUR/USD in range FTSE 100 to crack 6,400 on back of Draghi factor

FTSE 100 to crack 6,400 on back of Draghi factor Euro edges higher, holds near 3-week high as focus shifts to ECB

Euro edges higher, holds near 3-week high as focus shifts to ECB Dollar up on higher yields, euro hit by ECB’s ‘less for longer’ decision

Dollar up on higher yields, euro hit by ECB’s ‘less for longer’ decision