European Stimulus Sparks Bond Blitz

French utility GDF is the first company in over 14 years to issue euro bonds bearing no regular payments for investors

Investors snapped up a half-billion euros of French utility bonds that will pay them no interest, a groundbreaking deal that shows how corporations are rushing to take advantage of Europe’s efforts to keep interests rates low to try to revive the Continent’s economy.

Next to tap the market may be Berkshire Hathaway Inc., which plans to raise around €3 billion, or $3.4 billion, in its first euro-denominated bond sale as soon as Thursday, according to a person familiar with the company.

The €500 million bond sale by GDF Suez SA came a day before the European Central Bank was scheduled to spell out details of how it will buy €60 billion a month in government and corporate bonds to fuel economic growth by pumping money in the region’s financial system.

In anticipation, investors have piled into European debt markets, pushing yields on some government bonds below zero. Yields fall as bond prices rise. The GDF Suez deal raises the prospect that companies may soon find investors willing to accept negative yields on bonds, essentially paying the borrowers to hold their debt.

With government bonds that trade at negative yields, investors are betting that further price gains will make up for the lost interest.

European corporations have yet to issue bonds with a negative yield at the time of pricing, but the GDF Suez deal signals that it may happen soon.

“This is a perfect sign of just how substantial the spillover effect of the ECB’s asset-purchase program is,” said Jürgen Odenius, chief economist at Prudential Fixed Income, which manages $540 billion in assets. “Mario Draghi was unequivocal about the fact that the ECB will even buy bonds with a negative yield,’’ he said, referring to the president of Europe’s central bank. “And that of course creates huge opportunities for companies to price at the sort of level that GDF did.”

Last year, the ECB imposed negative interest rates on deposits by banks, another attempt to spur lending that pushed yields lower.

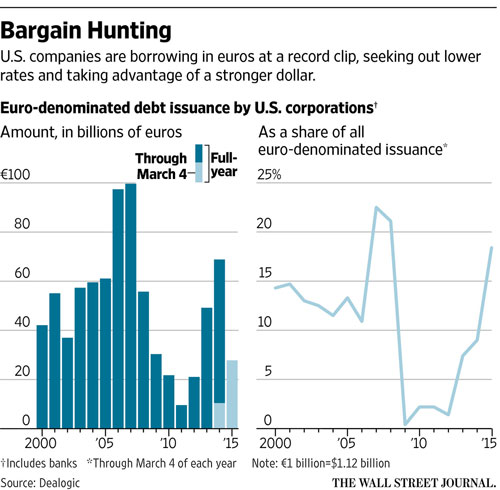

U.S. companies also have rushed to Europe to take advantage of falling rates.

Berkshire Hathaway, the conglomerate run by Warren Buffett, is raising money in Europe in part because of the low rates there and also to replace some U.S. debt that recently matured, the person familiar with the company said. The Omaha, Neb., conglomerate is looking for acquisitions in Europe, but Mr. Buffett has yet to find a deal he likes. In the meantime, the company will convert the euros to dollars and pocket the cash until it is ready to buy, the person added.

Some €26.6 billion of bonds from U.S. borrowers have been issued in Europe this year, with about a third of those coming from Coca-Cola Co.’s bumper bond sale last week, data from Dealogic show. Oreo cookie maker Mondelez International Inc. and breakfast-cereal maker Kellogg Co. are some of the other familiar names that have crossed the Atlantic to load up on cheap debt.

“It’s so cheap to borrow in euros that it’s a no brainer,” said James Athey, a fund manager at Aberdeen Asset Management in London. “It’s something we expect to see more and more of to the point where, potentially, U.S. corporates are issuing far less in their own market and issuing far more in Europe.”

The average yield for corporate bonds issued in euros is a near-record low 1.08%, according to a Markit index, more than a percentage point lower than a year ago.

GDF Suez sold its two-year, zero-coupon bond at a price that put the yield for investors at 0.13%. By contrast, the average yield for corporate bonds issued in dollars is 3.67%, Markit data show.

The €500 million was the most ever raised at 0% interest. The financing arm of Italian car maker Fiat issued a €10 million bond with a 0% coupon in 2001, according to Dealogic, and German auto group BMW sold €150 million of zero-coupon bonds in 1999.

In all, Paris-based GDF Suez sold four tranches of debt, with maturities ranging between two and 20 years, for a total value of €2.5 billion, according to bankers involved in the deal. The 20-year tranche of GDF Suez’s deal offers a coupon of just 1.5%, which also represents a record low for a corporate bond in euros of that maturity.

Euro-denominated corporate debt from some of the world’s biggest companies has been in hot demand as investors, hamstrung by subzero yields on many European government bonds, seek alternative assets to boost returns. That has pushed up corporate-bond prices, making it even cheaper for companies to borrow.

Investors say it makes sense for U.S. companies with European operations to borrow cheaply in Europe instead of raising cash in the U.S. and swapping it into euros.

“The reasoning to come to Europe is the same for most companies—it’s just a cheap source of funding,” said Bryan Wallace, a fund manager at J.P. Morgan Asset Management, adding that most of the deals have come from frequent borrowers that are just using the funds for general business purposes, rather than earmarking them for specific projects.

Even for those companies that have no European operations to finance, selling bonds in Europe is still attractive because the cost of borrowing in euros and swapping the cash back into dollars using a so-called cross-currency swap is around the lowest level on record, Mr. Wallace said.

Investors, too, stand to benefit from the rush to sell euro-denominated bonds.

“There are certain borrowers that have come to the European market that usually only issue in dollars, so it gives me an opportunity to add names in our euro-only funds that I don’t already hold,” Mr. Wallace said.

The ECB’s asset purchases, known as quantitative easing, could see the bank buy as much as €1 trillion of top-rated bonds in the eurozone.

“I don’t know if [the GDF Suez deal] marks the start of many more corporate bonds pricing with zero coupon, but it shows that it’s certainly very achievable for other issuers,” said Jeff Tannenbaum, head of the debt syndicate at Bank of America Merrill Lynch, one of the banks in on the French deal. “There is tremendous competition for assets at the moment and very high liquidity, which makes it possible for corporate to borrow, in some cases at record low levels.”

Source: WSJ – European Stimulus Sparks Bond Blitz