SNB:Monetary policy remains expansionary

The Swiss National Bank (SNB) is maintaining its expansionary monetary policy. The target range for the three-month Libor remains at between –1.25% and –0.25%, and interest on sight deposits at the SNB is unchanged at –0.75%. The Swiss franc is still significantly overvalued. Negative interest is making Swiss franc investments less attractive. At the same time, the SNB will remain active in the foreign exchange market, in order to influence exchange rate developments where necessary.

The global economic outlook has deteriorated slightly in recent months and the situation on international financial markets remains volatile. Against this background, the negative interest rate and the SNB’s willingness to intervene in the foreign exchange market serve to ease pressure on the Swiss franc. The SNB’s monetary policy is thus helping to stabilise price developments and support economic activity.

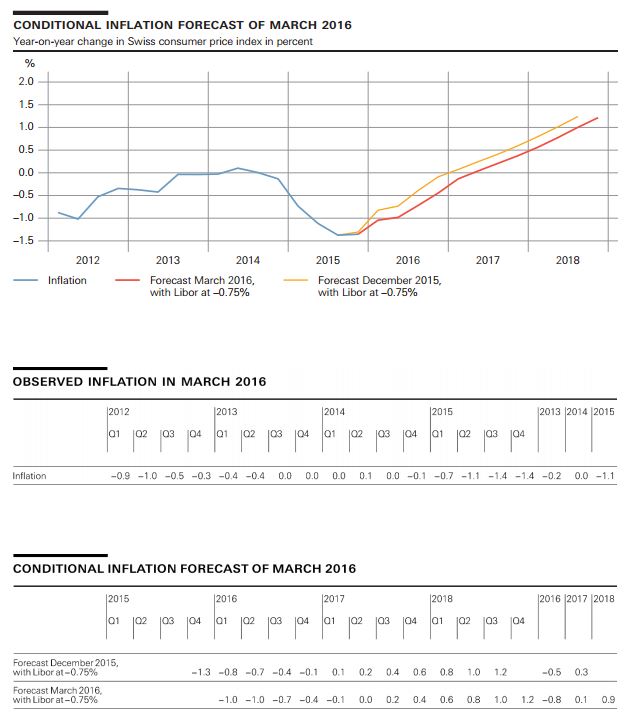

The new conditional inflation forecast has been revised downwards slightly compared to the previous quarter. The further drop in oil prices is contributing to a decline in inflation in the short term. In the medium term, the main factors dampening inflation are the globally low inflation levels and the lacklustre outlook for the global economy. The SNB continues to expect that inflation will re-enter positive territory in the coming year. It is projecting an inflation rate of –0.8% for 2016, compared with –0.5% in the December forecast. For 2017, the inflation forecast is at 0.1%, which is 0.2 percentage points lower than in the previous quarter, while for 2018 it is 0.9%. The conditional inflation forecast is based on the assumption that the three-month Libor remains at –0.75% over the entire forecast period.

Global economic performance at the beginning of the year was slightly weaker than had been anticipated at the quarterly assessment in December. Around the world, manufacturing and trade remained sluggish, contributing to a further sharp fall in oil prices. Against expectations, the low energy prices have had only a limited stimulatory effect on household consumer Berne, 17 March 2016 Press release Page 2/3 spending. By contrast, they have had a negative impact on the growth outlook in oilproducing countries, including the US.

These factors will continue to hold back the global economy over the coming months. Accordingly, the SNB’s assessment of the global economic outlook is somewhat less favourable than in December. The recovery in the advanced economies is expected to continue at a moderate pace. Growth in China is likely to slow further. Moreover, the prevailing risks are still considerable. The complex structural changes taking place in China could have negative repercussions for global demand. In Europe, structural weaknesses and political uncertainty could hamper economic development. Furthermore, renewed upheaval on global financial markets would impair financing conditions for households and companies.

In Switzerland, annualised real GDP increased by 1.7% in the fourth quarter. Thus, for 2015 as a whole, the Swiss economy recorded growth of just under 1%. This confirms the SNB’s assessment at the time of the minimum exchange rate discontinuation. However, the economic momentum is not broad-based. Profit margins are still under pressure at many companies, and the willingness to invest and the demand for labour remain commensurately subdued. Consequently, the unemployment rate has risen again slightly in recent months.

Since the SNB assumes a more modest pace of global economic growth, it is also expecting a slower recovery in Switzerland. For this year, it is anticipating GDP growth of between 1% and 1.5%, instead of around 1.5% as hitherto.

Over the last few quarters, the downward trend in real estate price momentum has been confirmed. Mortgage volumes have also recorded slightly slower growth. Yet the imbalances on these markets persist, due to comparatively weak growth in fundamentals. The SNB will continue to monitor developments on the mortgage and real estate markets closely, and will regularly reassess the need for an adjustment of the countercyclical capital buffer.

Source: SNB

Related Posts

Bank of Israel reports Monetary Policy for the six Months 0f 2016

Bank of Israel reports Monetary Policy for the six Months 0f 2016 Swiss National Bank leaves expansionary monetary policy unchanged

Swiss National Bank leaves expansionary monetary policy unchanged Swiss National Bank released: Monetary policy remains expansionary

Swiss National Bank released: Monetary policy remains expansionary- SNB says progress needed from biggest Swiss banks on capital

- Swiss National Bank discontinues minimum exchange rate and lowers interest rate to –0.75%