The dawn of financial technology in Islamic finance

Over the past decade, financial technology — widely referred to as FinTech — has grown primarily due to growing Internet access worldwide and the emergence of smartphones and apps.

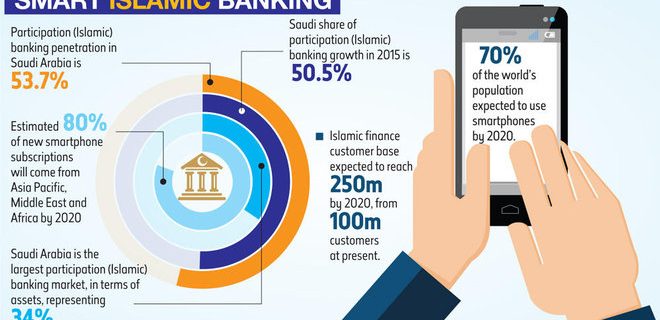

According to the Ericsson Mobility Report published last year, 70 percent of the world’s population is expected to be using smartphones by 2020.

As smart devices are increasingly becoming part of everyday life for most people in the digital age, it is essential for the banking sector to become more innovative to enhance its productivity.

“We’re transitioning toward a situation where growth for companies and economies will have to depend more on productivity than before,” said Jarmo Kotilaine, chief economist at the Bahrain Economic Development Board (EDB).

“To achieve that, you will need better management, better innovations, new distribution channels and new capital.”

Increasing the efficiency of digital banking will particularly serve customers in Saudi Arabia, where banks’ working hours overlap with those of most employees.

Comprehensive digital banking can save them a journey to the branch. Moreover, Saudi Arabia is a pioneer when it comes to technology penetration in the region.

“The usage of technology in Saudi Arabia is advanced, whether in retail banking, cash management or corporate,” said Talat Hafiz, secretary-general of Saudi banks’ Media and Banking Awareness Committee.

“When it comes to technology, what applies in conventional banking also applies in Islamic banking.”

He added: “Using financial technology improves the quality of the banking experience among clients. It influences the speed and accuracy of the experience. Technology makes products more reachable to clients.”

The change in behavior patterns among clients in the banking sector requires banks to respond to new customer needs and rethink how they deliver services to their clients, taking them to a phase of digital banking.

“As a matter of policy, we in SAMA (the Saudi Arabian Monetary Authority) encourage all regulated institutions to be responsive to the needs of their customers, and have always supported the development of products that meet those needs,” said SAMA Gov. Ahmed Al-Kholifey.

A report published this month by Ernst & Young (EY) said the adoption of financial technology is not an option anymore, but an essential requirement for Islamic banks to gain more market share.

As customer technology penetration in the Gulf Cooperation Council (GCC) increases, users are expected to become more familiar with using digital tools in their banking transactions, retail investments and peer-to-peer (p2p) lending and crowdfunding.

According to the EY report, Saudi Arabia, the United Arab Emirates (UAE) and Malaysia are the three largest Islamic banking markets in terms of assets.

Saudi Arabia takes the lead with 34 percent market share, followed by 17 percent and 13 percent in the UAE and Malaysia, respectively.

Ashar Nazim, partner in EY’s Global Islamic Banking Center, said the “FinTech revolution” — in terms of data, analytics, robotics and artificial intelligence — has the ability to bring scattered data together and help decision-makers make better decisions.

“We believe the last 20 years of Islamic banking have been about innovation in Shariah contracts and Shariah-compliant products,” said Nazim.

“The next 20 years will be about combining smart technology with Islamic banking in order to grow further.”

The size of the Islamic finance industry is now close to $2 trillion. “We believe there’s an additional trillion dollars in the industry which isn’t formally captured,” Nazim added.

He said this additional trillion dollars is primarily from endowments (waqf), high net worth and institutional investing done in a number of infrastructure projects in the conventional and Islamic markets.

“Bringing the additional $1 trillion into the Islamic finance industry is where FinTech can be very important,” Nazim said.

FinTech: A threat?

As financial technology is deemed to better facilitate banking services, it can also be seen as a disruption to the banking sector.

Looking at the history of Islamic finance, it was seen as a disruption to conventional finance.

“FinTech is now disrupting the overall finance world. The big banks are slower in adopting technology because they have a legacy to protect, but start-ups are more welcoming in adopting change,” Nazim said.

The EY report showed that in FinTech space in the GCC, Islamic finance is still in “dismissive mode,” thinking it is not going to impact the industry.

Nazim said the mindset has to change: “We have to start thinking as a start-up, and that requires a complete change in behavioral economics, in terms of how organizations are run.”

He added: “Bringing smart technology by itself is of no use unless the organization’s culture changes. Islamic banks are in better positions because they’re smaller than conventional and more local. It’s easier for them to change.”

FinTech can open doors for further national and international collaboration in the banking industry.

There is a growing realization within banks that they cannot afford to do everything by themselves.

“There has to be collaboration within the industry. At the moment collaboration is at a national level, and in future it will be at cross-country level. The next 20 years will be collaborating in terms of smart technology,” said Nazim.

“FinTech shouldn’t be seen as a threat or as competition. There is tremendous potential for collaboration between the GCC and Malaysia in FinTech.”

He added: “These smart technologies increase levels of trust and the speed with which you do these transactions.”

Speaking at the recent World Islamic Banking Conference (WIBC) in Bahrain, Rasheed Mohammed Al-Maraj, governor of the Central Bank of Bahrain (CBB), said the smart use of technology is a game-changer in banking, just as in other aspects of daily life.

“Technology has made it possible to access more customers, in a more comprehensive way, at a lower cost, than in the past,” he said.

“Islamic banks must make full use of these technological enhancements and invest more in this space.”

Al-Maraj added: “The CBB believes in embracing new technology, and will soon be issuing regulations to facilitate FinTech solutions. We’d like to see Islamic banks come forward and take the lead in this area. FinTech is leading the way.”

According to SAMA’s Al-Kholifey, all the 12 banks operating in Saudi Arabia offer Shariah-compliant finance, as do several branches of foreign banks that are licensed to operate in the Kingdom.

“Saudi retail banking is overwhelmingly comprised of Shariah-compliant products, and we note significant growth of Shariah-compliant growth in the corporate sector as well, growth that we expect to see continue in the next decade,” he said.

EY says the introduction of FinTech will increase the Islamic finance customer base, which is roughly 100 million today, to 250 million by 2020.

“So more than twice the growth in customers can be achieved with the adoption of FinTech,” Nazim said.

Source: Arab News