Payment token derivatives: the risks behind the hype

Compared to a direct investment in Bitcoin, for example, an investment in derivatives with payment tokens as underlying assets is more transparent but is by no means risk-free. Many of the risks associated with payment tokens have an impact on derivatives. And there are other risks as well – such as issuer default risk.

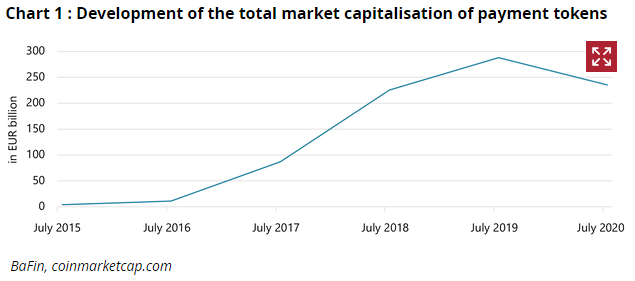

Investors have shown an unwavering interest in investments in payment tokens such as Bitcoin – also commonly known among investors as “virtual currencies” or “crypto currencies”. This trend is also evidenced by the figures: the total market capitalisation of all existing payment tokens increased almost sixtyfold between 2015 and 2020 (see Chart 1). The number of different payment tokens has also grown rapidly in recent years. According to publicly available sources, there are currently more than 6,000 payment tokens in circulation. On the other hand, a large number of them have a very short lifespan or are largely unknown and therefore of no value.

The growing interest among retail investors is not limited to direct investments in payment tokens. There is also a rise in demand for financial instruments deriving their value from the performance of payment tokens.

The number of securities issued with payment tokens as underlying assets has increased from 12 securities as of 2018 to around 6,500 securities today. In this area, the trading volume among retail investors in Germany has been worth more than EUR 700 million over the last two years. The derivatives industry expects the demand for such financial instruments to increase further.

However, these products are not suitable for every investor. They pose significant risks, especially for retail investors.

What are payment token derivatives?

Derivatives are financial instruments whose price depends on the performance of an underlying. Two classes of derivatives are particularly relevant for retail investors: contracts for difference (CFDs) and certificates.

CFDs involve a contract between two parties to bet on how the price of a particular underlying will evolve. Due to significant investor protection concerns, BaFin adopted a product intervention measure with its general administrative act of 23 July 2019, thereby restricting the marketing, distribution and sale of CFDs to retail clients in Germany (see “CFD trading” announcement). Due to the high volatility of crypto assets, these CFDs are subject to a stricter leverage limit. Retail clients in Germany are permitted to only trade CFDs with such underlyings with a leverage of up to 1:2 (initial margin protection).

Certificates and exchange-traded notes are bearer bonds. These financial instruments grant the holder the right to claim, from the issuer, the payment or repayment of an amount of money or the delivery of an underlying (see expert article “Nice name, nasty surprise” on the BaFin website).

What are payment tokens?

Payment tokens are digital investments which are not financial instruments as defined in section 2 (4) of the German Securities Trading Act (Wertpapierhandelsgesetz – WpHG). In addition, they do not constitute legal tender and do not grant any rights. There is no central institution responsible for these virtual currencies, such as a central bank, that supervises them or issues the units. Information technology typically plays a significant role here: encryption technology is used to secure the payment tokens while decentralised networks are used to manage them (see issue 1/2018 of BaFinPerspectives).

The definition of payment tokens does not cover security tokens that have security-like features. Security tokens are classified as securities. As a result, the issuers of such tokens are subject to regulatory requirements, such as the obligation to draw up a securities prospectus. There are currently no known examples of security tokens or stablecoins serving as underlyings for derivatives.

Well-known payment tokens include Bitcoin, Ether, Litecoin, Ripple, Tether and Bitcoin Cash. Bitcoin accounts for more than 60% of the total global market capitalisation of payment tokens (EUR 235 billion). It is no surprise that it is also the most common underlying for derivatives.

What opportunities do investments in payment tokens have to offer?

The way in which the value of a payment token evolves usually does not depend on other macroeconomic factors. There is often no correlation between payment tokens and traditional asset classes such as equity indices and commodities. Due to this lack of correlation, investors try to diversify their portfolio with payment tokens and thus reduce their overall risk exposure. In general, however, payment tokens mainly serve as a speculative investment for experienced investors.

What are the risks associated with investments in payment tokens?

It is almost impossible for investors to reliably forecast the performance of payment tokens due to the high level of complexity of virtual currencies. This is due in particular to the fact that payment tokens have no real economic value. They have no intrinsic value and are therefore prone to speculation. The reputation and acceptance of a payment token is extremely important for the token’s stability, especially given that payment tokens are not issued by central banks and are not legal tender.

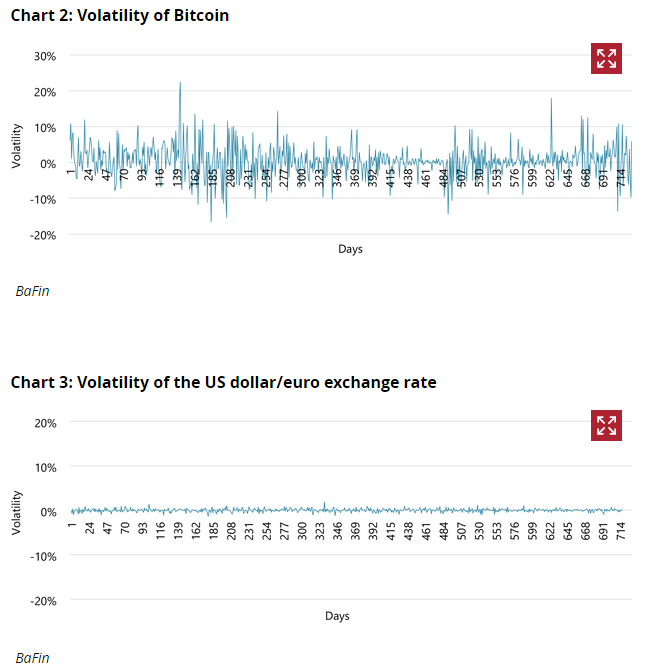

The extreme volatility of payment tokens is another risk to be mentioned here (see info box). The volatility of well-known payment tokens is usually 6 to 13 times higher than that of other underlyings. For example, Bitcoin is 26 times more volatile than the US S&P 500 stock market index – not on the basis of changes in contractual rights, but mainly on the basis of speculation.

Definition

Volatility

Volatility refers to the degree of variability in returns. It is a measure of the frequency and intensity of fluctuations in the value or price of an underlying. Thus, volatility is also a measure of the uncertainty surrounding an investment and its price risk. The higher the volatility, the more the price fluctuates and the more risky an investment is.

The extreme volatility of Bitcoin also becomes evident when compared to currencies: between July 2017 and July 2019, its average volatility was more than 4% (see Chart 2). Over the same period, the volatility of the US dollar-euro exchange rate was 0.36% (see Chart 3). Bitcoin thus fluctuated twelve times more.

Furthermore, the exchange rate between the US dollar and the euro fluctuated between two consecutive closing prices by a maximum of 1.88% during the period under review, while the value of Bitcoin changed several times by more than 10%. On 7 December 2017, the closing price was 22.44% higher than the closing price of the previous day. These significant short-term flash crashes are still typical of payment tokens today.

Ledger splits are also typical. This is when a payment token is split and the two resulting blockchains that share a common history continue. This is usually followed by higher volatility and uncertainty about the future price of both the payment token that is retained and the newly created one. In addition, there is a risk that a payment token ceases to exist, which means that the derivative no longer has an underlying and therefore becomes worthless. Moreover, payment tokens are not regulated. There is no independent body in charge of monitoring trading or pricing. As payment tokens are not financial instruments under the WpHG, they are not subject to the requirements regarding back office activities and transparency under capital market law, as opposed to most underlying assets such as shares.

One way for investors to manage their crypto assets themselves is wallets. This is where the private key granting full access to the crypto assets is held. Wallets exist in the form of software or hardware, such as a USB stick, or the sheet of paper on which the key has been written down. If investors lose their private keys, they will no longer be able to access their crypto assets. There is also the risk of a total loss if hackers crack the password. In order to reduce technical risks, investors may rely on service providers conducting crypto custody business. In this case, the management of their crypto assets is similar to the management of securities in a securities account.

The European Supervisory Authorities (ESAs) and BaFin have already warned against the risks associated with crypto assets.

What are the advantages of payment token derivatives?

In the best possible scenario, investors can make use of derivatives to benefit from the rising prices of payment tokens – or benefit from falling prices, if they have bet on the opposite. With payment token derivatives, they can speculate on an investment while avoiding specific operational or technical risks because they are not purchasing the token directly. In principle, this makes the investment simpler and less prone to error. For example, if investors opt for derivatives, the payment token does not need to be stored in a wallet with a private key.

Overall, trading in payment token derivatives is more transparent than a direct investment in such tokens. This is due to the legal requirements, in particular for certificates. Certificate issuers are required to draw up not only a prospectus, but also a key information document. These documents describe the risks of the investment, including information on the tradability of the certificate and on the costs associated with the product, as well as a risk classification and a recommended holding period. In addition, the issuer classifies products based on the target market. However, this increased amount of transparency relates only to the certificate structure – the underlying itself remains unclear.

What are the disadvantages of payment token derivatives?

In contrast to the direct purchase of payment tokens, it should be noted that investors bear not only the price risk of the underlying but also the risk of issuer default, as for all certificates, and counterparty default risk in the case of CFDs.

In addition, the market risks of the tokens are transferred to the relevant derivative. There is also no guarantee that trading can be continued on the basis of supply and demand in the case of payment token certificates. As there is often a lack of liquidity or insufficient market breadth, market makers set prices at their own discretion, with the option of suspending or even terminating the quotation of prices at any time (see expert article “Market making” on the BaFin website). In addition, the issuer includes in the price any costs they incur as a result of hedging or acting as a market maker. Such costs do not arise in the case of a direct investment in payment tokens.

The leverage effect of turbo certificates or the possibility that the issuer will terminate investment certificates at short notice are inherent risks that investors need to bear in mind as well, depending on the design of the derivative contract they opt for.

What should investors bear in mind?

Payment tokens have no intrinsic value and are not subject to supervision under the legal provisions governing securities. They are characterised by high volatility and thus uncertainty about their future performance.

It is true that certificates, in particular, are generally more transparent and allow investors to participate in the performance of payment tokens without having to invest in them directly. However, the high level of uncertainty due to the volatility of such tokens also has an impact on the derivatives that are based on these tokens. Moreover, the issue surrounding the general lack of transparency of payment tokens also persists in the case of certificates and CFDs.

Payment token derivatives are therefore unsuitable for a long-term investment strategy but are suitable at best for short-term speculation. Since it is particularly complicated to forecast the future price developments of payment tokens, only experienced investors should consider investing in derivatives with these underlyings.

Independently of this, BaFin monitors the market for certificates with payment tokens as underlying assets and examines on a case-by-case basis whether supervisory measures, which may even lead to a product ban, are necessary.

Source: BaFin

Related Posts

The German Supervisory Authority Released Guidelines On CFDs Trading

The German Supervisory Authority Released Guidelines On CFDs Trading- Breaking: BaFin restricts CFD trading

BaFin has published a report on FinTechs: Young IT companies on the financial market

BaFin has published a report on FinTechs: Young IT companies on the financial market Bitcoin and the Fintech Sector Are Being Scrutinized by Mexican Legislators

Bitcoin and the Fintech Sector Are Being Scrutinized by Mexican Legislators Algorithmic markets would save us from another financial crisis

Algorithmic markets would save us from another financial crisis