China Prepares Mergers for Big State-Owned Enterprises

Plan seeks to make firms more profitable but tightens government’s grip

China’s leadership is preparing to radically consolidate the country’s bloated state-owned sector, telling thousands of enterprises they need to rely less on state life support and get ready to list on public markets.

The economic slowdown has heightened the imperative to eke better returns out of the state firms that tower over China’s economy, from the giants that dominate oil, banking and other strategic sectors, to smaller ones that run hotels and make toothpaste.

But instead of scaling back their role, as called for by economists both inside and outside China, the plan could tighten the state’s grip over economic activity and make already inflated behemoths even bigger.

Communist Party leaders plan to release broad guidelines in the next months for restructuring the country’s more than 100,000 state-owned enterprises, according to government officials and advisers with knowledge of the deliberations.

The leadership is determined to “crack a hard nut,” said Li Jin, deputy head of the China Enterprise Reform and Development Society, a trade group under the top regulator of state firms.

Strategically important industries such as energy, resources and telecommunications are marked for consolidation, the officials and advisers say. The merged entities would then be reorganized as asset-investment firms, with a mandate to make sure they run more like commercial operations than arms of the government.

Upper management will be under orders to maximize returns and prepare many of the companies for eventual listing on stock markets, say these people.

State companies are already under pressure to hand the government 30% of their profits by 2020—from 15% or less now. Some of this is to be earmarked for costs related to a rapidly aging population. The new plan adds a goal of making the biggest state companies profitable enough to go public by 2025, according to the officials.

By many measures, the state sector has grown more dominant in China’s economic life, despite recurring calls from Beijing to build a more vibrant private sector for continued prosperity.

The plan could be controversial as it falls short of the steps advocated by some market-reform advocates: For one thing it takes large-scale privatization off the table.

“The idea of having asset managers oversee state assets is a good one, but it shouldn’t be done through combining existing state-owned enterprises that are already so big,” says Zhang Wenkui, a deputy director at the Development Research Center of the State Council, China’s cabinet. “That would only lead to less competition.”

The State-owned Assets Supervision and Administration Commission, or Sasac, which oversees the largest state enterprises, declined requests for comment on the reform plan. In a speech to the legislature last week, Premier Li Keqiang vowed to “deepen the reform of state-owned enterprises.” He pledged to “speed up efforts” to set up state-asset investment companies, though he didn’t elaborate.

The Wall Street Journal reported last month on a facet of the restructuring: plans to merge state oil companies to reduce what officials see as wasteful competition at home to make them more viable globally. The restructuring program goes farther by repackaging merged entities as investment firms to prepare them for public listing.

Beijing still sees a bigger role for the private sector: The plan supports efforts to invite private investment into state firms, though, the officials and advisers say, private investors wouldn’t be permitted to hold controlling stakes in most state firms.

In order to reduce the waste, corruption and unaccountable management that have plagued the sector, Beijing sees a combination of mergers, better supervision and the discipline of public listing as crucial, Chinese officials say.

“State-owned enterprises should have the kind of governance and financial accountability that meets the criteria for publicly traded companies,” Guo Shuqing , governor of China’s eastern Shandong province and a former financial regulator, told reporters while attending the nation’s annual legislative session this weekend.

State firms have thrived on access to loans from state banks and government-set rules that limit competition from private businesses, which complain of being muscled out of the market unfairly. Economists have said the special status has come at a cost to Chinese taxpayers and consumers.

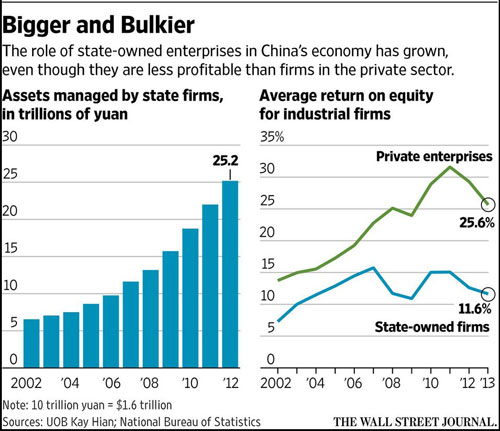

In an analysis for The Wall Street Journal, economist Zhu Chaoping at UOB Kay Hian Holdings Ltd., a Singapore-based brokerage, found that assets at state-owned enterprises, defined as those majority-controlled by the government, jumped 90% to 25.1 trillion yuan ($4 trillion) in 2012 from 2008. Return on equity among state-controlled manufacturers, however, averaged 11.6% in 2013, compared with nearly 25.7% for their private brethren, according to Mr. Zhu’s analysis.

When drawing up the new state-sector reform plan, senior Chinese officials looked at Singapore’s holding company for state firms, Temasek Holdings, according to the officials and advisers. Under the Temasek model, the government would confine itself to the role of a stakeholder, receiving dividends but leaving day-to-day running of the companies to professional managers at the asset-investment firms hired at market rates.

Beijing’s plan stops short of that. The government will retain its current practice of naming senior management teams for the newly formed companies, the officials and advisers say.

Beijing has quietly started experimenting with forming state investment companies through merging existing ones. Last year, Sasac picked State Development & Investment Corp. and Cofco Corp. for such a trial. At the regulator’s direction, State Development & Investment, a financial and industrial conglomerate, scooped up a securities firm while Cofco—one of China’s largest food-processing firms—swallowed another state-owned food company. Cofco absorbed the assets of China Huafu Trade & Development Group “for free,” according to Huafu, which became a subsidiary.

Officials at the regulator, State Development and Cofco declined to comment.

Meanwhile, in the nuclear power sector, China Power Investment Corp. is merging with the State Nuclear Power Technology Corp., according to the securities filings made by China Power’s listed arms last month.

Making big state companies bigger is likely to draw renewed wrath from private Chinese companies and from Western businesses and their governments, which have criticized Beijing for years for essentially subsidizing state firms by giving them preferential access to credit, land and other resources.

Combining state firms would “run counter to” Beijing’s promise to broaden private participation in the economy, said Zhang Ming, an economist at the Chinese Academy of Social Sciences, a government think tank.

Source: WSJ – China Prepares Mergers for Big State-Owned Enterprises