FCA Thematic Review: Best Execution and Payment for Order Flow (‘PFOF’)

Financial Conduct Authority (FCA) Thematic Review: Best Execution and Payment for Order Flow (‘PFOF’)

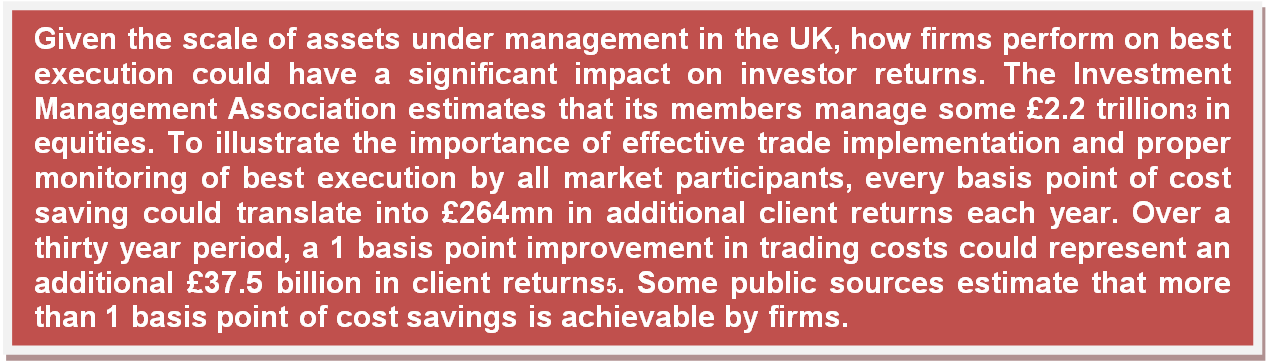

FCA thematic review of best execution and Payment for Order Flow (‘PFOF’) found that many firms do not understand key elements of FCA requirements and are not embedding them into their business practices.

There are two main messages from FCA work:

FCA review identifies a significant risk that best execution is not being delivered to all clients on a consistent basis.

- Most firms are not doing enough to deliver best execution through adequate management focus, front-office business practices or supporting controls.

- Firms need to improve their understanding of the scope of their best execution obligations, the capability of their monitoring and the degree of management engagement in execution strategy, if they are to meet our current requirements.

- All firms also need to prepare for the challenges of MiFID II implementation in this area.

Supervisory findings for Best Execution are summarised below:

1. Scope: There was a poor level of understanding of which activities are covered by the obligation to provide best execution. Frequent attempts were made by firms to limit the scope of the obligation in their dealings with clients, often through the use of general ‘carve-outs’ which are not permissible or through continued reliance on out-dated market conventions.

2. Monitoring: Most firms lacked effective monitoring capability to identify best execution failures or poor client outcomes. Monitoring often did not cover all relevant asset classes, reflect all of the execution factors which firms are required to assess or include adequate samples of transactions. In addition, it was often unclear how monitoring was captured in management information and used to inform action to correct any deficiencies observed by firms.

3. Internalisation and connected parties: Firms which relied heavily on internalisation or on executing orders through connected parties were often unable to evidence whether this delivered best execution and how they were managing potential conflicts of interest. Firms were also unable to show how they separated explicit external costs incurred on behalf of clients from internal costs or how their commission structures for internalisation avoided discriminating against other venues.

4. Accountability: It was often unclear who had responsibility and ultimate accountability for ensuring that execution arrangements and policies met our requirements. Despite the significant volume of change in European markets since 2007, firms were still conducting only cursory reviews of policy documents which did not address the full scope of their best execution obligations. Moreover, these were largely focused on process rather than delivering client outcomes and often lacked front-office engagement.

To read the FCA thematic review: FCA Report TR14-13 (3)