Big Banks Struggle to Pass Fed’s ‘Stress Tests’

Bank of America must resubmit proposal to address certain weaknesses

Four of the biggest names on Wall Street struggled to pass the Federal Reserve’s 2015 “stress tests,” and the U.S. units of two foreign banks fell short, underscoring the constraint the annual exercise imposes on the largest banks more than six years after the 2008 crisis.

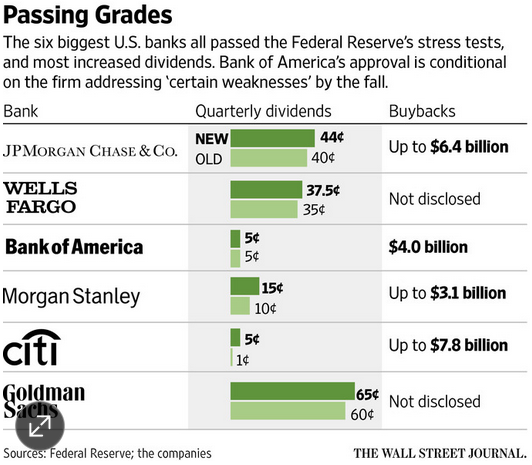

Goldman Sachs Group Inc., J.P. Morgan Chase & Co. and Morgan Stanley received the green light to return income to investors only after adjusting their initial requests to ensure capital buffers stayed above the minimums required by the Fed.

Bank of America Corp. got conditional approval to return capital to shareholders after the Fed found “certain weaknesses” in its ability to measure losses and revenue and in other internal controls. The bank can temporarily reward investors by boosting dividends or share buybacks, but it must submit a revised plan addressing its shortcomings by Sept. 30. If the Fed isn’t satisfied with the bank’s progress, it can freeze the capital distributions.

The Charlotte, N.C., bank said it would increase stock buybacks but hold dividends steady. It was the only lender among the six biggest U.S. banks to not raise that payout. Bank of America Chief Executive Brian Moynihan said the lender was “committed” to submitting a revised plan “in the time frame the Fed has established.”

Bank regulators have steadily raised capital requirements for the largest banks since the crisis in an effort to make banks—and the financial system—more resilient and better able to absorb losses. The changes have forced banks to fund themselves with less borrowed money and more investor cash, such as common equity that can’t flee when market turmoil strikes.

“Our capital plan review helps ensure that the capital distribution plans of large banks will not compromise their ability to continue lending to businesses and households even during a period of serious financial stress,” Fed governor Daniel Tarullo, the central bank’s point man on regulatory issues, said in a statement.

Still, the fact some big banks needed to take a so-called mulligan and adjust their capital plans is likely to stoke criticism that the Fed’s process is too opaque and designed to find shortfalls at banks rather than ensuring they can build up the necessary capital to absorb losses.

“The regulators are incrementally penalizing the largest banks more,” said CLSA analystMike Mayo. If Congress wants the Fed to be harder on the biggest banks, “they’re following through.”

Fed officials say they don’t want the tests to be predictable, because firms should plan for unforeseen risks. They say allowing firms to adjust their plans before determining whether they pass or fail is designed to ensure banks aren’t surprised by the Fed.

The changes by J.P. Morgan, Goldman Sachs, and Morgan Stanley kept their capital levels above the Fed’s required minimums, but it wasn’t immediately clear whether they would reduce the amount of money the firms return to shareholders overall. The banks that disclosed dividends and buybacks didn’t indicate whether those were in line with their original requests to the Fed. Morgan Stanley pared back its plan slightly, according to a person familiar with the matter.

Despite the foreign banks’ failures and broader struggles, analysts said the tests were largely positive for Wall Street, since all the U.S. domestic banks passed the exercise for the first time since 2009. After adjusting their capital plans, all 31 banks were found to be adequately capitalized and able to keep lending during a market shock—the first time no bank has fallen below a Fed minimum.

This year’s test, which gauges whether banks could keep lending during periods of severe economic stress, went to the heart of Wall Street’s trading operations, a factor that appears to have contributed to the big banks’ difficulties.

The six largest firms had to weather a global market-shock scenario that included corporate bankruptcies and a sharp drop in the price of risky securities, such as loans to highly indebted companies. Market volatility was greater than in previous years’ tests, producing relatively higher losses for banks heavily engaged in capital-markets activities—like buying and selling equity and debt instruments, Fed officials said. Goldman, Morgan Stanley and J.P. Morgan all have large trading operations.

One big bank, Citigroup Inc., had an easier time than in years past. The bank earned Fed approval for its capital plan, a major victory for Chief Executive Michael Corbat, who made passing the exam a top goal after the firm in 2014 failed for the second time in three years. Mr. Corbat had said he would step down if Citigroup failed again.

Citigroup said it won approval to raise to five cents a share its quarterly dividend, which has been one cent since the financial crisis. It can also buy back up to $7.8 billion of its own shares, up from last year’s level of $1.2 billion.

The Fed rejected the capital plans of the U.S. units of Deutsche Bank AG and Banco Santander SA for “qualitative” deficiencies including in their abilities to model losses and identify risks. The two firms can’t increase dividend payments to their parent firms or other shareholders, but can continue to pay at last year’s levels. Deutsche Bank said it didn’t request any dividend payments, while Santander said it had permission to keep a dividend it declared in January.

After the Fed’s results were announced, many of the big banks, including J.P. Morgan and Morgan Stanley, highlighted their strengthened conditions and said they were pleased to be returning cash to shareholders.

Lloyd Blankfein, Goldman’s chairman and chief executive, said the bank is “focused on managing our resources dynamically, growing our client franchise, and generating superior returns for our shareholders while remaining well capitalized.”

Banks appear to be improving at meeting the Fed’s expectations, and the test results “are going to become nonevents for the industry as we go forward,” predicted Gerard Cassidy,an analyst with RBC Capital Markets.

The results come as investors have been pressing the biggest banks to improve their shareholder returns, which have lagged behind the broader market since the crisis. Analysts and frustrated investors have floated the idea that certain banks would be worth more broken into pieces. Bank executives have rejected that premise.

Dividends at big banks have been restrained in recent years. The 23 banks in the S&P 500 that take the stress tests had an aggregate indicated dividend of $45.3 billion at the end of 2007, or about 18% of the total for all firms in the index, according to S&P Capital IQ data analyzed by Reality Shares Inc., a dividend-focused investment firm. As of March 6 of this year, the figure was $26.4 billion, or about 7%.

Deutsche Bank’s unit, which took the stress test for the first time this year, was rejected for “numerous and significant deficiencies” across several areas of the capital-planning process, including the bank’s ability to identify risks, the Fed said. The bank said in a statement that it is “committed to strengthening and enhancing its capital planning process.”

Santander failed the stress test for the second year in a row due to “widespread and critical deficiencies across” its planning procedures, the Fed said. The Fed’s description of the bank’s shortcomings was identical to last year’s, identifying, among other issues, problems with internal controls and risk management.

The chief executive of Santander’s U.S. unit, Scott Powell, said the results show the bank can weather a severe economic downturn without dipping below the Fed’s capital minimums. “However, the qualitative assessment highlights that we still have meaningful work to do to meet our regulator’s expectations and our own standards of excellence,” he said in a statement.

Source: WSJ – Big Banks Struggle to Pass Fed’s ‘Stress Tests’