Prices are going to rise — and fast!

With stockmarkets barely ruffled, few are thinking beyond the very short-term and they are mostly guessing anyway. Other than possibly the very short-term as we emerge from lockdowns, the economic situation is actually dire, and any hope of a V-shaped recovery is wishful thinking or just brokers’ propaganda. But for now, monetary policy is to buy off all reality by printing money without limit and almost no one is thinking about the consequences.

Transmitting money into the real economy is proving difficult, with banks wanting to reduce their balance sheets, and very reluctant to expand credit. Furthermore, banks are weaker today than ahead of the last credit crisis, and payment failures on the June quarter-day just passed could trigger a systemic crisis before this month is out.

Sooner or later bank failures are inevitable and will be a wake-up call for markets. Monetary inflation will then become an obvious issue as central banks and government treasury departments become desperate to prevent an economic slump by doing the only thing they know; inflate or die.

Foreigners, who are incredibly long of dollars and dollar assets will almost certainly start a chain of events leading to significant falls in the dollar’s purchasing power. And when ordinary Americans finally begin to discard their dollars in favour of goods, the dollar will be finished along with all fiat currencies that are tied to it.

Introduction – monetary transmission problems

Between different schools of economics there is much confusion over the link between changes in the quantity of money and prices, exposed afresh by the collapse in GDP due to COVID-19 and the aggressive monetary response from the authorities to contain the economic consequences.

Neo-Keynesians appear to understand the link exists, but for them inflation is always of prices which can be managed by adjusting monetary policy subsequently.

Monetarists follow a mechanical quantity theory leading to a relatively straightforward relationship between changes in the quantity of money and of prices after a time lag of a year or so. The principal difference with the neo-Keynesians is in the timing: monetarists see monetary inflation occurring long before the price effect, and neo-Keynesians in charge of central bank monetary policy assume rising prices can be controlled subsequently by varying interest rates.

The Austrian school, which is banished from these proceedings, explains that inflation is of money and nothing else, and the effect on the general price level is determined by a combination of changes in the money quantity and of consumers’ relative preferences for holding money relative to goods.

But central banks operate exclusively on neo-Keynesian lines. They feel free to expand the money quantity so long as the general level of prices does not exceed a targeted 2%; except when it does there is usually an excuse not to restrict money supply growth immediately. Keynesian Inflationism offers problems on so many levels, not least being it is rather like driving a vehicle using a rear-view mirror for guidance. But importantly for our analysis, central banks do not seem to realise current monetary policies guarantee the death of their currencies.

Central bankers act as if money supply increases after prices, which is what monetary policy amounts to. They have other nonsensical beliefs, such as through an inflation tax despite robbing consumers of their wealth, it stimulates them to buy. Whoever thought that one up as a lasting policy beyond short-term distortions deserves an Ignoble prize for idiocy.

Ah! That was Lord Keynes. And perversely, his disciples are today’s main recipients of the Nobel prize for economics. We are now seeing central banks, like some latter-day Aztec priests, trying to appease their gods with human sacrifices. We are the sacrifices, lesser mortals trying to do the best for our families and ourselves, being slaughtered by monetary means.

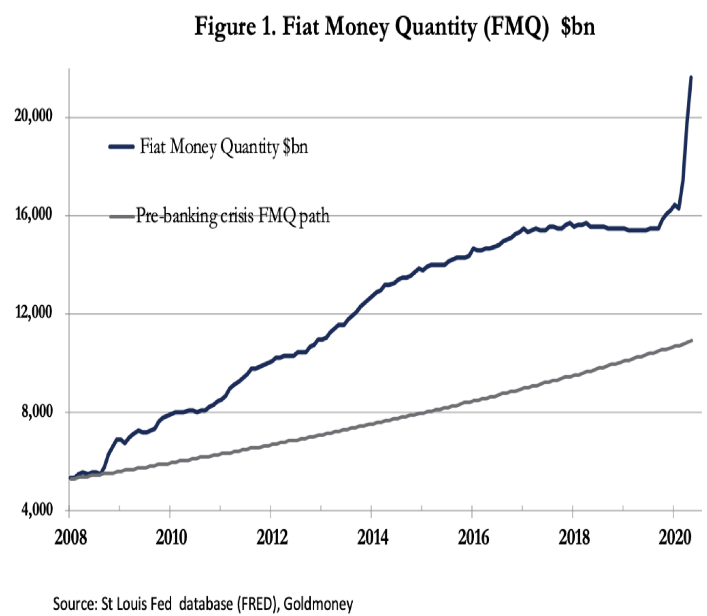

Figure 1 indicates the alarming debasement of our savings, earnings, and pensions so far through monetary expansion and explains why the dollar’s purchasing power has been declining faster than the CPI suggests.

The fiat money quantity reflects not only money in circulation, that is to say true money as defined by Austrian economists, but additionally the banks’ deposit reserves held at the Fed, the last data being for 1 May. It captures fiat money both in circulation and theoretically available for circulation.

From 2009 it shows the excess monetary inflation that followed the Lehman crisis in 2008, which until 1 February this year grew at an annualised monthly compound rate of 9.5%, compared with the pre-Lehman average long-run rate of about 5.9%.

No wonder independent analysts calculating the rate of price inflation tell us that it is running at 8%—10% (Shadowstats.com and Chapwood Index), instead of the CPI’s 1.5—2.0%. And if that was not bad enough, the recent sharp increase at an annualised rate of 98% since March comes on top of it, putting FMQ at more than double where it would be if Lehman had not happened. FMQ now also exceeds GDP, telling us there is more fiat money than US output, and yet more liquidity is demanded through the banks by failing businesses.

The Fed has increased base money at an unprecedented rate to provide liquidity, allegedly for the non-financial sector. For this to get to businesses banks must be prepared to increase their lending to non-financials and bank credit must not contract. But as Figure 2 shows, bank balance sheets have stopped growing and even contracted since the end of April.

Between 26 February and 29 April bank balance sheets increased by $2,489bn. These figures include the uplift in total reserves held at the Fed and not in public circulation, which over the same period increased by $1,083bn. Therefore, banks increased their other assets by $1,406bn between these dates. Those other assets are split between financials and non-financials, the evidence of rising financial asset prices relative to commercial business’s decline strongly suggesting Wall Street has been favoured over Main Street

Subsequently, up to 17 June bank balance sheets contracted by $169bn. The extent to which banks are increasing financial activities will be balanced by an even sharper contraction in bank credit for non-financials than indicated by the overall balance sheet.

Central banks with their reliance on inflation now have a problem: the banks are failing to pass on extra money to the non-financial sector by expanding their balance sheets. Yet, the disruptions to supply chains, the onshore component totalling some $38 trillion and an unquantifiable offshore component feeding into it, are still there and their problems are growing by the day. In short, we face a continuing liquidity crisis with limited means of relieving it.

Economic prospects for the next few months

Before we proceed in our analysis of the price effects of inflation, we must assess the economic outlook,as the backdrop to the likely consequences for the scale of monetary inflation, and then we can have a stab at evaluating the effect on prices.

The first clue is in Figure 2 above, which shows that bank lending is contracting, and it is important to understand why. At this stage of the credit cycle, which began expanding following the aftermath of the Lehman crisis over a decade ago, a sharp contraction of bank credit to non-financials is normal. It is what drives periodic recessions slumps and depressions, and monetary stimulus by central banks is intended to help commercial bankers recover their mojo and resume lending.

The relevant history of central bankers’ attitudes to bank credit goes back to Irving Fisher’s description of how contracting bank credit intensified the 1930s depression by the liquidation of debt, forcing collateral values down and leading to bank runs and the bankruptcy of thousands of banks. Ever since, monetary policy is guided by the fear of a repeat performance. But the Keynesian stimulus at the start of the credit cycle only increases the destabilising nature of bankers’ behaviour, consisting of long periods of growing greed for profitable loan business, interspersed by sudden reversions to fear of loan risk. It results in a cycle of credit expansion and contraction, which in recent cycles have been resolved temporarily by increasingly aggressive expansions of base money along with government actions to support ailing industries.

It is a sticking-plaster approach which allows the wound to fester out of sight.

Following Lehman’s failure, a similar pattern to the one unfolding today of a rapid increase in bank assets through the newly invented QE was followed by a contraction of bank credit which lasted about fifteen months. But that crisis was about financial assets in the mortgage market, which had knock-on effects in the non-financials. Difficult though it was, its resolution was relatively predictable.

This crisis started in the non-financials and is therefore more damaging to the economy; its severity is likely to lead to a banking crisis far larger than the Lehman failure and possibly greater than anything seen since the 1930s depression.

Commercial bankers are now waking up to this possibility. For them, the immediate danger is associated with this quarter-end just passed, when demand for credit to pay quarterly charges increases significantly. Already, businesses are in arrears as never before, with many shopping malls, office blocks and factories unused and rents unpaid. It is this problem, shared by banks around the world, which due to the severity of current business conditions is likely to tip the banking system over the edge and into an immediate crisis. The extent of the problem is likely to be revealed any time in this month of July.

Excluding the subsequent effects, the Lehman crisis cost the US Government and its agencies over $10 trillion in support and rescue operations. This time, being in the non-financial sector with knock-on effects for the financial economy, this crisis is much deeper than Lehman and will require a far larger bailout cheque for collapsing industries. Part of the problem are the broken supply chains needing bridging finance. And none of this can be done without the Fed funding it all directly or indirectly through quantitative easing. Despite the massive monetary inflation already underway there can be no doubt that aggregate consumer demand and the production of goods to satisfy it will take an enormous hit this year and beyond, and there is little doubt about the state’s will be on the hook for even more monetary financing.

Unemployment of previously productive labour is already rising dramatically, and as bankruptcies increase the rise in the unemployment numbers will continue to do so. Let us therefore assume that compared with last year the production of goods and services and consumer demand for them will decline by at least 25%. Note that we avoid using money-totals, since they are meaningless; it is the exchange of labour being converted into physical products and services that matters.

Into this situation is injected enormous quantities of money, none of which defeats the constraints on true supply of goods, nor for overall demand in a high unemployment economy. Put in a more familiar way, we will have too much money chasing not enough goods. There is only one outcome, other things being equal; the purchasing power of the dollar in terms of consumer goods will be driven significantly lower. But central bank analysis rules this out, associating too much money chasing too few goods with only an expanding, over-stimulated economy.

This explains stagflation, the situation where an economy stagnating in overall demand is accompanied by rising prices. Nor are other things ever equal, the condition for the paragraph above. The early receivers of inflated money will spend it, driving up the prices of the goods and services they acquire before the prices of other goods and services are affected. These early receivers include the Federal Government, which in an election year is doubly unlikely to hold back. Distribution of state money will increasingly be in the form of welfare to the unemployed, skewing spending towards life’s essentials. Inevitably, in an economy with subdued activity not responding quickly enough to produce the volumes of products desired, prices, mainly of essential items, will increase sharply.

Almost certainly, a broad index of prices will not capture this secular effect until too late. The CPI includes a majority of items which are only occasionally bought by individuals. Poor demand for non-essentials where there is now an oversupply puts downward pressure on their prices even in an inflationary environment. It is therefore possible for the CPI to record little or no price inflation as an average when food and energy prices are rising strongly, particularly when statistical methods designed to show little or no increase in price inflation are additionally taken into account.

Consequently, central banks are already being badly misled by the CPI’s statistical method. And when prices for essentials are soaring, they will continue to increase the quantity of money in circulation, distracted by that 2% increase in the CPI target. By the time it creeps up above that rate it will be too late, much monetary water having already flowed under the bridge.

The politicians will likely dismiss rising prices for food and fuel as the result of profiteering — they always do and then contemplate introducing price controls, making this outcome even worse.

Let us stand back from what is happening — or shortly will be — and estimate the inflation scene as far as we know it:

• After growing at an average annual rate of 9.5% since the Lehman crisis, broad money in the form of FMQ accelerated to an annualised growth rate of 98% from February this year. Bank balance sheets increased by just under $2.5 trillion in March and April but are now beginning to contract. More increases in base money from the Fed are sure to follow, compensating for lack of bank credit expansion.

• The Fed is underwriting the whole US corporate debt market in an attempt to ensure the flow of finance for all borrowers, bypassing the banks and suppressing yields in the markets. The secondary market for non-financial debt in the US alone is $9.6 trillion, probably requiring an initial trillion or so of Fed buying in the foreseeable future to keep yield spreads suppressed.

• The quarter-end two days ago will be marked by a significant rise in missed payments. But demands for more bank credit will be resisted by the banks leading to many more existing loans going sour. Under the weight of non-performing loans, it will be a miracle if a banking crisis is not triggered by missed payments in the US, or elsewhere where banking systems are even weaker. Wherever it starts, the Fed is committed to underwrite the whole US banking system, along with all its commercial borrowers with falling sales and disrupted supply chains, to prevent unemployment spiralling out of control. The monetary inflation required for this alone could easily be at least twice the cost of the Lehman crisis.

• The Fed is also attempting to underwrite the whole market for financial assets by inflating the quantity of dollars being fed into it in order for the necessary financial and economic confidence to be maintained.

• Monetary expansion on this scale is bound to undermine the dollar in the foreign exchanges as foreigners liquidate portfolio investments, US Treasury stock, agency stock and the excess of bills and bank deposits not required for reserve currency liquidity purposes. This will leave the Fed funding a government deficit escalating beyond control, and if it is to keep borrowing costs low, it must also absorb sales of foreign-held Treasury and agency debt which currently total $6.77 trillion.

Measured in current dollars, even the quantity of narrow M1 money after all this inflationary financing is likely to grow to much more than 2019’s US GDP, which will be contracting sharply in terms of physical output and consumption. This is the recipe for a monetary collapse, as John Law illustrated in France in 1720.

Government finances

Apart from keeping the banking system up and running, the other of the Fed’s overriding objectives is to ensure the US Government is funded. There can be no doubt that its budget deficit is already out of control. Before COVID-19, the White House was already on course for a trillion-dollar plus deficit. That has widened as a result of tax shortfalls and increased spending costs. In May, the Congressional Budget Office estimated the deficit for the first eight months of fiscal 2019/20 had more than doubled to $1,905 billion, of which $1,162 was incurred just in April and May. If the deficit continues at this rate, then the outturn for the fiscal year will at least $3 trillion.

The administration had proposed a $2 trillion stimulus, some of which is reflected in figures for April and May. Congress went even further, proposing a $3 trillion stimulus. If elements of Congress’s extra spending are adopted, we can amend our expectations and pencil in a budget deficit rising towards $4 trillion at an annualised rate.

The belief that funding sums of this magnitude in the markets can be achieved at current interest rates is a fallacy. It can only be attempted with unlimited monetary creation, which ultimately undermines this solution.

Before the virus hit, it was estimated by the White House that annual borrowing costs would be $422 bn. If the deficit increases by $3 trillion, this will rise to about $480bn on the White House’s current interest rate assumptions. With the interest rate burden already accounting for over 40% of the pre-COVID-19 budget deficit estimates, we can see why the Fed and US Treasury are keen to keep bond yields suppressed. In a nutshell, if they rise a funding crisis is the only result.

Following a near certain banking crisis there is bound to be a flight out of deposits and risk assets into the perceived safety of US Treasuries. For a brief period, the government will be able to fund its deficit without a rise in interest rates. But unless the increased issue of Treasury bonds is bought by the Fed, the economic effect will be to drain funds from the financial and non-financial private sectors. Therefore, the Fed is almost certain to cover almost all of it by quantitative easing.

In summary, government finances started in this presidential election year with the largest deficit on record. We now have an economic disaster unfolding, driven not only by the COVID-19 lockdowns but by a confluence of a turn in the bank credit cycle and rising trade protectionism. It is no exaggeration to suggest we are on the brink of an economic catastrophe; a descent into an economic dark age. Not only is the budget deficit escalating to multiples of that expected as recently as last March, but there is no prospect of it declining at any time.

To this outlook we can add other negative factors. The contraction of cross-border trade globally is indicative of a spreading slump in business activity. The trend for increasing trade protectionism by America is growing. The retreat into nationalistic isolation is spreading. These trends are plain to see for those who care to observe them. And for America, in a presidential election year political factors are likely to make things even worse.

How monetary inflation translates into higher prices

We can expect to see two stages in the process of the dollar’s purchasing power being undermined. The first appears to have already commenced with the dollar weakening in the foreign exchanges, and the second, yet to come, is a public rejection of it as a means of exchange.

A year ago, foreign holders on the last reported figures held over $20.5 trillion of US securities to which must be added bank deposits, bills, CDs etc., totalling a further $6,452bn for a total of almost $27 trillion. The contraction in cross-border trade and the isolationism that goes with economic downturns suggest that foreigners now require smaller dollar balances, leading to the repatriation of dollar funds into foreign currencies.

Also compelling foreigners to sell are political developments. The Trump administration has been destabilised by its failure to contain the coronavirus with lockdowns, and a socialistic Joe Biden is now ahead in the opinion polls. If Biden is elected, then all the dollar’s gains during the Trump administration could be lost.

We must also not forget that unless the US’s savings rate increases, in normal times a higher budget deficit leads to matching higher trade deficits. When monetary capital arising from trade deficits is recycled, the budget deficit becomes funded directly or indirectly by foreigners. Indeed, this is why foreigners have accumulated dollars and dollar investments significantly in excess of US GDP. But if this virtuous circle is disrupted, the twin deficit still exists without the net dollar proceeds in foreign hands continuing to accumulate. Instead, the dollars are sold for other currencies and commodities.

Therefore, foreigners have two separate dollar problems to consider: the level of their current holdings which are now too high, and the increasing quantities of dollars in their hands from current and future trade. And with the budget deficit escalating towards $4 trillion, the trade deficit will increase to a similar amount. Unless, that is, the American people increase their savings. They might do so for the very short-term as a reaction to rising economic uncertainty, but not on the scale required, nor for long enough to make a significant dent in the twin deficit relationship.

In his remaining months as president, Trump is likely to respond to a rising trade deficit by increasing tariffs on increasing quantities of imported goods, extending his trade policy against China to other jurisdictions. If so, production costs for consumer goods will rise, driven by a combination of a falling dollar in the foreign exchanges and escalating tariffs on imported goods. It then becomes a vicious circle with foreigners seeing their dollar earnings collapsing in value, encouraging them to liquidate more of their existing holdings.

The price effect of these factors is bound to be noticed eventually by American consumers and will affect the relative preference individuals will have between holding a monetary reserve and owning goods. A small change in the aggregate level of consumer preferences in this regard can have a significant impact on prices, and if they desire collectively to hold less liquidity and more goods, prices of commonly desired goods will rise sharply. With COVID-19 and changing economic conditions, preferences are likely to increase for essentials, particularly food and energy, and with capacities for essential products deprived of the capital required to expand output the ability of manufacturers to respond by increasing production will be badly restricted.

In the final stages of an inflation driven crisis the general public becomes indiscriminate in their purchases of goods, even to the point of selling property in order to survive. A currency which no one wants then loses all its objective value for transaction purposes.

This is what happens following all monetary inflations. Once the general public loses confidence that a fiat currency will retain its objective value in transactions, it begins to dispose of it as rapidly as possible and it is too late to stabilise it. This has been the experience of every fiat currency which has died in the past.

The text-book example was the great inflation in Germany’s post-war Weimar Republic. Then, as is increasingly the case today, the government relied on monetary inflation as its principal source of funding. The final collapse, when the German people no longer accepted the paper mark as money for transactions, took place between about May and November, taking roughly six months. The time taken was a combination of an understanding of what was happening spreading throughout the economy and the foreign exchanges, and the time taken to obtain cash — which was in short supply due the demand for it — and find the goods, which were also in short supply, to buy. It was described at the time as the crack-up boom, the final boom into goods and real values that marks the end of a seemingly endless inflation, being the complete breakdown of a monetary system.

Today, the time taken for the dollar’s final descent into oblivion will be set by the same human values, quickened by today’s instant communications and payment systems, potentially making the collapse more rapid.

In conclusion, don’t be misled by the common belief that a decline in the US economy will lead to falling prices. The inflationary response from the Fed, which will be immense, will ensure far too much money ends up driving demand for a diminished quantity of needed goods.

By Alasdair Macleod, www.goldmoney.com

Find more: Contributing Authors