Credit cycles and gold

The Trump shock produced some unexpected market reactions, partly explained by investors buying into a risk-on argument,equities over bonds and buying dollars by selling other currencies and gold.

The Trump shock produced some unexpected market reactions, partly explained by investors buying into a risk-on argument,equities over bonds and buying dollars by selling other currencies and gold.

This is because President-elect Trump has stated he will implement infrastructure investment and tax-cut policies. If he pursues this plan, it will lead to larger fiscal deficits, and higher interest rates. The global aspect of the markets recalibration focuses on the strains between the dollar on one side, and the euro and the yen on the other, both still mired in negative interest rates. The capital flows obviously favour the dollar, and are putting the Eurocurrency markets under considerable strain.

Gold has been caught in the cross-fire, being a simple way for US-based hedge funds to buy into a rising dollar by selling gold short. While this pressure may persist, particularly if the euro weakens further ahead of the Italian referendum, it is essentially a temporary market effect. This article explains why this is so by analysing the next phase of the credit cycle, and the implications for interest rates and prices, which will be fuelled by higher US fiscal deficits in addition to China’s stockpiling of raw materials. It concludes that there are factors at work which were originally identified by Gordon Pepper, who was acknowledged as having the finest analytical mind in the UK Gilt market in the 1960s and 1970s.

Pepper observed that banks were consistently bad investors in short-maturity gilts, almost always losing money. The reason, he explained, was banks bought gilts when they were averse to lending, and sold them when they become more confident. This meant banks bought government bonds when economic confidence was at its lowest, bad debts in the private sector had risen, and interest rates had fallen to reflect the recessionary environment. These were the conditions that marked the high tide in bond prices.

As surely as day follows night, recovery followed recession. As trading conditions improved, corporate takeovers became common as businesses repositioned themselves for better trading prospects, and a period of increasing industrial investment followed. The banks began belatedly to sell down their gilt positions to provide capital for economic expansion. By the time banks felt confident enough to lend, markets had already anticipated higher demand for credit, as well as a more inflationary outlook. Inevitably, banks ended up selling their gilts at a loss.

Pepper had identified the mechanics behind bank credit flows between financial and non-financial sectors, an important topic broadly overlooked even today. Currently, the credit cycle has become prolonged and distorted, because most of the accumulated malinvestments that would normally be eliminated in the downturn phase of the credit cycle have been allowed to persist, thanks to the Fed’s aggressive suppression of interest rates. Consequently, bank credit was never reallocated from unproductive to more productive use, but has been added to and extended in the name of financial engineering.

Things are about to change. President-elect Donald Trump has stated that he will expand government spending on infrastructure and at the same time cut taxes, in which case he will set in motion a new expansionary phase for the US economy, leading to an additional increase in bank credit. The immediate effect has been to drive up bond yields and increase expectations of higher dollar interest rates.

Working from Gordon Pepper’s thesis, the banks are only in the initial stages of mark-to-market bond losses, since they have yet to sell down their bond holdings to create lending room for infrastructure expansion and a sharply higher fiscal deficit. That will not happen before next year, assuming Trump follows through on his economic plans. But markets can be expected to increasingly discount future bond sales by the banks and other financial intermediaries before then, and given that yields fell to unusually low levels ahead of Trump’s expansionary plans, bond losses can be expected to be correspondingly greater.

The new expansionary phase

President-elect Trump is in effect advocating a substantial fiscal stimulus to the economy. The difference between monetary stimulus and fiscal stimulus is found in price inflation. Simply put, monetary stimulus tends to inflate asset prices, while fiscal stimulus tends to inflate consumer prices. Therefore, fiscal stimulus leads with greater certainty to rising interest rates and bond yields, because of the price inflation effect, inflicting painful losses for banks invested in bonds.

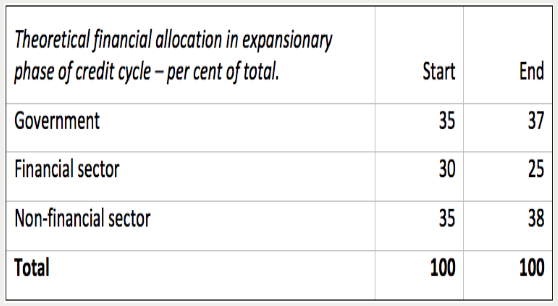

The change from monetary to fiscal stimulus can be expected to undermine asset prices, for reasons that will become clear. The following table illustrates the flows that can arise from fiscal stimulus of the economy, and puts Pepper’s theses in a clearer light.

Government spending increases over the cycle, reflecting fiscal stimulus, in this example from 35% to 37% of the economy. And because the fiscal stimulus is spent in the non-financial private sector, that increases as well. Inevitably, the financial sector, representing money that’s employed in purely financial activities, gets squeezed, in this case falling from 30% to 25% of the economy. Financial activities can be said to deflate.

While actual numbers will differ from this theoretical example, it illustrates that in the expansionary phase money must leave purely financial activities. You cannot have both fiscal stimulus and a reallocation of economic resources into the non-financial private sector without creating a powerful deflationary effect on financial assets. Consequently, not only will bond yields rise, but equity markets will be impacted as well, at the very point where fundamentals for equities appear to be at their best. Today’s equity market euphoria is therefore a reflection of improved sentiment, ahead of the reality.

Keynesians would argue that the strains faced by the financial sector can be offset by credit expansion. Initially, this may be the case, so long as banks have room on their balance sheets for additional credit growth. However, the inflationary effects of fiscal expansion on consumer prices become a considerable and relatively immediate force, rapidly dominating monetary policy considerations. This is due to the fiscal deficit being directly translated into increased demand for goods and services through government spending, driving up prices as the extra money created out of thin air is spent. The result is interest rates are inevitably raised by the central bank to protect the purchasing power of the currency.

Probably the clearest example in living memory of this effect was the UK economy in the first half of the 1970s, which prompted Pepper’s analysis. From 1970 onwards, the Heath government reflated aggressively by depressing interest rates and increasing fiscal stimulus. The result was a stock market boom that ended in May 1972, gilt yields having bottomed earlier that year. As the economy improved, gilt yields rose further, and equities entered a deep bear market. The Bank of England increased interest rates, while gilt yields rose, equity prices fell, and price inflation increased. Speculation migrated from equity markets into commercial property, when rents and capital values responded to expanding office demand, driven by the artificial economic boom.

Eventually price inflation accelerated to the point where interest rates had to be raised further, triggering a collapse in the commercial property market, necessitating the rescue of the lending banks associated with it. Over the course of the cycle, the Bank of England’s base rate had increased from 5% in September 1971 to 13% in November 1973, precipitating the commercial property crash. Long-dated gilt yields had more than doubled to over 15%, and the equity market lost 75% of its value by the end of 1975. The British Government’s financial position was so bad, she had to borrow money from the IMF.

All the signs of a similar cycle are emerging today but on a grander scale, with Donald Trump intending to pursue the expansionary fiscal policies of Edward Heath. But there are obvious differences, particularly the high burden of debt in the private sector. In the 1970s private sector debt levels were low, so much so that residential property prices in the UK were broadly unaffected by rising interest rates. Today, residential property prices at the margin typically reflect 80% loan-to-value mortgages. Indeed, the level of private sector debt in America is now so great that a rise in the Fed Funds Rate to between two and three percent may be enough to crash both residential property prices and the US financial sector with it.

Another important difference is the interconnectedness of markets. Rising yields for US Treasuries are certain to be transmitted into rising yields in other currencies, particularly for the Eurozone. The Eurozone’s banks, whose currency’s very survival could be threatened by these developments, will face bond losses potentially so great that the whole European banking system could collapse. The ECB is likely to continue to pump money into the financial sector in a desperate attempt to save the banks, but it can only do so much before the price-inflation effect of a falling euro forces it to raise interest rates as well.

Britain, along with everyone else in the seventies, as well as the US in the coming years, also had a specific problem in common, rising commodity and energy prices. Artificial demand generated by fiscal expansion in the US in the 1970-74 era contributed to a significant increase in the general level of commodity prices. Most notable was the increase in the price of oil, as OPEC ramped it up from $3 to $12 per barrel in 1973 alone. Rising commodity prices were paid for by monetary expansion, just like today. And today, China is pursuing vast infrastructure plans for all Asia, which requires her to stockpile and use unprecedented quantities of industrial raw materials and energy. Trump’s expansionary plans will clash with China’s far larger plans, driving up commodity prices measured in dollars even further. This is in addition to the substantial gains seen so far, making a bad price outlook even worse.

The effect on gold

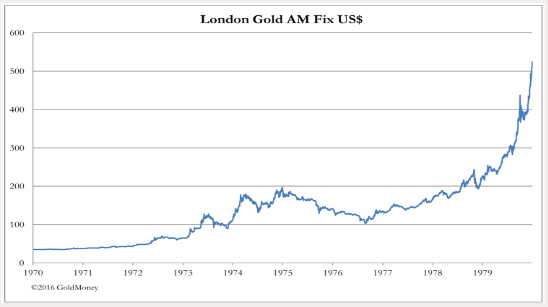

The chart below shows how the gold price behaved in the 1970s.

Gold rose from $35 to $197.50 between 1970 and the end of 1974, an increase of more than four times. During that period, as mentioned above, the Bank of England’s base rate rose from 5% to 13%. The Fed’s discount rate was 4.5% in 1972 and rose to 8% in August 1974. So, a rising gold price was accompanied by a rising interest rate, contradicting the conventional wisdom of today. Gold went on to hit a peak price of $850 at the afternoon fix of 21 January 1980, when the Fed’s discount rate was at an elevated 12%.

The current belief that rising interest rates are bad for gold was disproved by those events. The reason gold rose had little to do with interest rates, and everything to do with accelerating price inflation. The only way a rising gold price could be halted was to raise interest rates high enough and sharply enough to collapse economic activity, which is what Paul Volcker did in 1980-81. In other words, until the Fed abandons all pretentions to supporting economic growth, people will continue to increase their preferences for owning goods over holding dollars, thereby continuingly reducing its purchasing power.

Another way of looking at the prospective gold price is to think of it in terms of raw material prices, which tend in the long run to be more stable when measured in gold, than when measured in fiat currencies. Given the outlook for commodity prices, as both China and America compete for raw materials and expand the quantity of money to pay for them, the gold price is more likely to maintain a level of purchasing power against rising commodity prices, instead of it declining with paper currencies. China has prepared herself for this event, having embarked on a longstanding policy of stockpiling gold since 1983. The amount she has accumulated in addition to declared reserves is a state secret, but my estimate is at least 20,000 tonnes. In 2002, the State had presumably secured enough physical gold for itself to allow its own citizens to join in, because that is the year the Peoples Bank established the Shanghai Gold Exchange, and the ban on private ownership of gold in China was lifted.

Over the last fourteen years, private individuals and businesses in China have accumulated at least another 10,000 tonnes, and China has become the largest producer and refiner of gold by far. We can truly say that China has prepared herself and her citizens well in advance for the collapse in purchasing power of the paper currencies that her demand for commodities is likely to engender. The only thing she must do is to get rid of her accumulation of US Treasuries before they become worthless, which she is now doing.

America, by contrast, is wholly unprepared for higher commodity prices. Her gold reserves, assuming they are as stated, are insufficient to underwrite a declining dollar, and in any event conversion into gold is not on offer to holders of dollars. In terms of commodity demand, America will be playing second fiddle to China in the coming years anyway, only making a bad price situation potentially worse.

Because of continuing non-cyclical Chinese demand for commodities, there is a significant risk that not even a debt-liquidating slump brought about by significantly higher interest rates will kill price inflation in western currencies. Unlike the 1970s, when the dollar was the tune to which all the others danced, China Russia and all nations tied to them by trade no longer dance exclusively to the dollar’s tune. Consequently, US monetary policy no longer exercises absolute control over global price inflation, measured in fiat currencies.

Price inflation pressures could therefore persist, despite a US debt-liquidating slump. The possibility that the price environment for the dollar will continue to be inflationary in a US economic slump, despite the Fed’s monetary policy, cannot be ruled out. But before that possibility is put to the test, the likelihood of a systemic collapse in the Eurozone is a more immediate and threatening risk.

Conclusion

We currently face the prospect of a reallocation of capital from America’s financial sector into government and non-financial activities, driven by President-elect Trump’s expansionary plans. These plans, if pursued, will lead to money flowing from purely financial activities and will have a profoundly negative effect on asset prices. Furthermore, price inflation, the result of fiscal expansion, will raise consumer prices to unanticipated levels, forcing the Fed to raise interest rates more than expected today. This article has pointed out why rising interest rates in the expansionary phase of the credit cycle do not undermine the gold price, unless, and this is no longer certain, interest rates are raised to the point where the US economy is driven into a slump. However, the world is no longer dependant solely on US economic and monetary factors, because Asian demand for industrial materials has become the principal engine of commodity demand. We can therefore no longer be sure a Volcker-style shock from the Fed will kill price inflation at the end of the upcoming expansionary credit cycle.

As all experience from the past clearly demonstrates, it is a mistake to believe that the gold price is set solely by dollar interest rates, or its relative strength in other currencies. This being the case, the current weakness of the gold price is simply a reflection of temporary dollar shortages, and nothing more.

By Alasdair Macleod, www.goldmoney.com

Find more: Contributing Authors