The Terrifying Truth About Negative Interest Rates

Pushing interest rates below zero is both an act of desperation and something that in theory should have a huge, immediate impact of the behavior of borrowers and savers. The fact that negative rates have become the new normal in big parts of the world but haven’t caused the expected behavior change should scare the hell out of everyone.

To understand why this is so, think of the rate of interest as the price of money. It’s what an individual or business has to pay to get credit with which to buy and invest. As with anything else, when the price of money is high, we tend to acquire less of it and when the price is low we acquire more. So making money not just cheap, not just free, but actually profitable to borrow, while making savings unprofitable to hold should, according to conventional Keynesian economics, create a scene in the credit markets reminiscent of those Black Friday Wal-Mart videos where fistfights break out over the last remaining Barbie Doll. Businesses in particular should be borrowing and investing like crazy, igniting an epic capital spending boom.

But that hasn’t happened. In Europe, for instance, negative rates have been in place for five years …

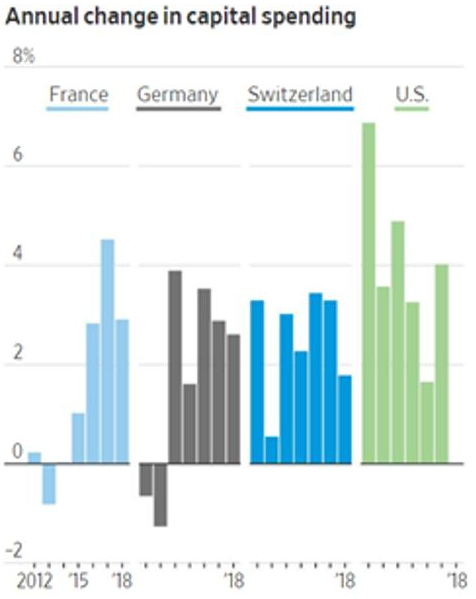

… and instead of a rip-roaring post-Great Recession recovery, the result has been the kind of anemic growth that conventional economics would predict for a tight-money environment. Business capital spending, the engine that in theory should be propelling Europe’s economy, looks like the opposite of a boom.

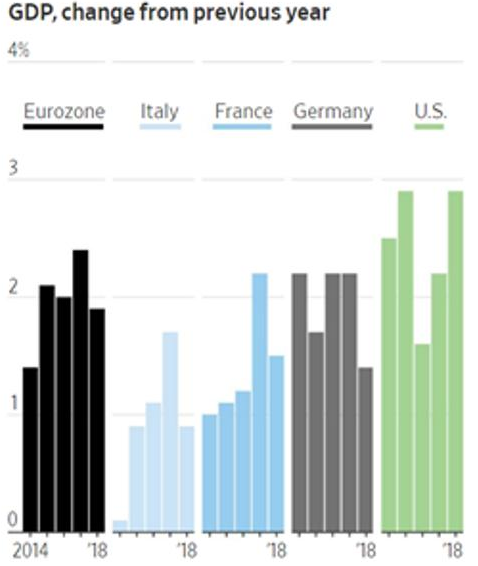

This translates into seriously boring GDP growth:

Why call such an uneventful situation terrifying? Because of what comes next.

Europe’s current sub-2% average growth rate is too slow to stop debt-to-GDP from rising. In other words, even with negative interest rates the Continent continues to dig itself ever-deeper into a financial hole. The same death spiral dynamic is in place in US, Japan and China.

To put the problem in more familiar terms, the world’s central banks have launched their version of tactical nukes at the problem of slow growth and soaring debt, and the dust has cleared to reveal the enemy unscathed and coming back for another go.

The next recession will begin with interest rates already at emergency levels, leaving central banks with no choice but to launch even bigger nukes. If interest rates are currently at -0.5%, then push them down to -5%. If buying up every investment-grade bond didn’t work last time around, then buy up junk bonds and equities, and maybe pay off everyone’s mortgage and student loans.

This will also fail, for reasons best explained by the unfortunately non-mainstream Austrian School of economics. The Austrians focus on a society’s balance sheet and observe that when low-quality (that is, speculative) debt exceeds certain levels, there’s nothing to be gained by encouraging more borrowing. So go ahead and cut interest rates to any crazy level you want. The inevitable, necessary result of too much bad debt is a crash that wipes that debt out. Or a hyperinflation that destroys the currency with which desperate governments flood the market in an attempt to stave off the debt implosion.

This explains why today’s negative interest rates haven’t ignited a boom (there’s already too much bad paper circulating), and also why the next round of monetary experiments will fail even more spectacularly than its predecessors.

By John Rubino, http://dollarcollapse.com/

Find more: Contributing Authors